Introduction: From Payment Pipe to Platform

You’ve built the foundation. Treasury operations are optimized. Stablecoin pay-ins and pay-outs are running. Your platform sends and receives cross-border payments with compliance embedded and reconciliation automated.

But there’s a structural gap still in place. Merchants and business clients interact with your stablecoin flows through external wallets. They on-ramp elsewhere, off-ramp elsewhere, and manage their stablecoin balances on a separate platform. Every time a user leaves your ecosystem to manage a balance, execute a conversion, or initiate a transfer, that activity and that revenue belongs to someone else. You’re running their payment flow, but you don’t have visibility into, or revenue from, the broader financial picture.

Embedded wallets change the model at its root. Give every customer a stablecoin wallet that lives inside your platform, and everything that was previously happening externally collapses into your ecosystem. Balances are held in-platform. Conversions happen in-platform. Payments to suppliers, yield on idle balances, and invoice settlements all run inside your UX, governed by your policy rules, and reconciled through your reporting infrastructure.

User accounts via non-custodial embedded wallets transform your role from a payment pipe that money flows through into the platform where money lives. Customer funds stay in your ecosystem longer. Value-added services become possible. The relationship with your customer deepens.

Non-custodial means the merchant or business client holds their own keys. You facilitate wallet creation, governance, and the transaction experience, but you don’t take custody of the funds. That distinction matters: no custody license is required to operate this model, which removes a significant regulatory barrier and keeps the operational responsibility clearly on the right side of the line.

This blueprint provides a practical, step-by-step implementation guide for transforming your business model to become a one-stop payments platform.

Use Case: Embedded Wallet User Accounts

The Problem

For PSPs: Merchants transacting in stablecoins rely on third-party wallets to manage their balances. Every time they leave your platform to handle a conversion, initiate a payout, or access a financial service, you lose visibility into that activity and miss the associated revenue opportunity. Your platform facilitates the payment but doesn’t capture the relationship.

For B2B payment providers: Business clients manage their stablecoin treasury externally, across separate providers with separate compliance processes. You have a clear view of the payment flow, but not the full financial picture of the clients you’re serving.

Embedded wallets solve both problems with the same architecture: every merchant or business client gets a stablecoin wallet inside your platform, provisioned automatically at account creation, with no external wallet setup required.

A Step-by-Step Operational Blueprint for Implementing User Accounts

Step 1: Deploy Embedded Wallets

Integrate non-custodial embedded wallet infrastructure into your platform using SDKs for web, iOS, and Android.

At the UX layer, wallet creation is invisible. A merchant or business client logs into their account, and a wallet is provisioned automatically in the background. Authentication uses passkeys: fingerprint or face scan on mobile, hardware key on desktop. There are no seed phrases, no private key management, and no blockchain knowledge required. The wallet appears to the user as an account feature, not a separate crypto product.

At the infrastructure layer, MPC architecture delivers sub-second signing speed. Wallet interactions execute in real time, with no latency impact on checkout flows or real-time invoice settlement. The architecture is non-custodial by design: the merchant or business client holds their own keys. You facilitate wallet creation and the transaction experience, but you do not take custody of their funds.

Gasless transactions remove a layer of operational complexity. Users don’t need to hold native network tokens to transact. Your platform sponsors gas fees, which means wallet interactions work even if the user has no familiarity with blockchain fee mechanics, and eliminates the support burden of helping users troubleshoot gas-related failures.

Wallet provisioning scales programmatically. As your merchant or client base grows, wallets are provisioned at scale through the same API that manages account creation. There’s no manual wallet setup per user.

For PSP deployments: every merchant gets an embedded stablecoin wallet that connects to the pay-in infrastructure you already have in place. Merchants receive stablecoin pay-ins into their wallet, hold balances, and initiate payouts, all within your platform UX.

For B2B deployments: every business client gets an embedded wallet that connects to the pay-in and pay-out infrastructure you set up previously. Invoice settlement, supplier payouts, and working capital management happen in-platform rather than externally.

Step 2: Configure Wallet-Level Governance and Compliance

Embedding wallets without governance is not a viable option for regulated payment operations. Every embedded wallet needs the same policy enforcement that governs your existing payment flows.

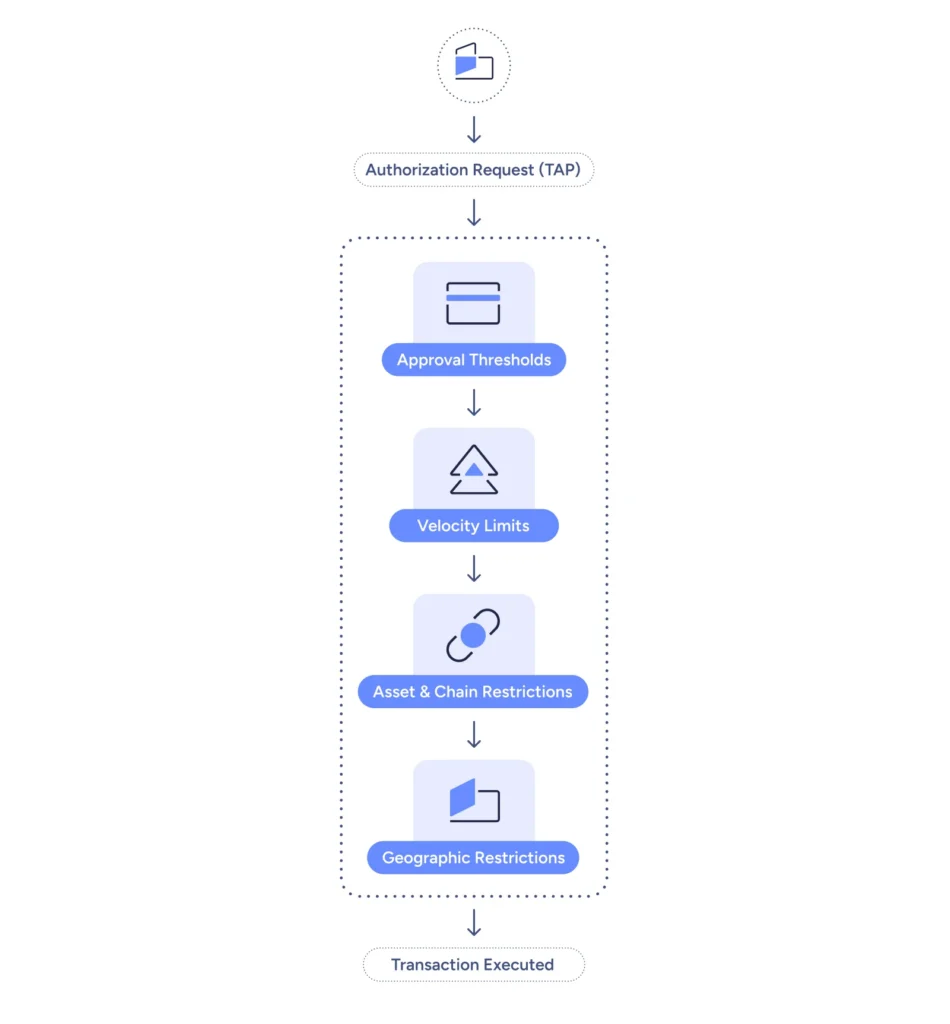

Configure Transaction Authorization Policy (TAP) at the wallet level:

Compliance screening runs on every transaction from every embedded wallet, with the same AML, sanctions, and Travel Rule controls that govern your pay-in and pay-out flows. This is the same Policy Engine that runs your existing infrastructure, now applied at the wallet level. That consistency matters: your compliance posture doesn’t fragment as you scale the number of active wallets.

Segregation of duties applies across wallet administration, transaction approval, compliance oversight, and policy management. The same governance principles that govern institutional treasury operations apply here, scaled to your full merchant or client base.

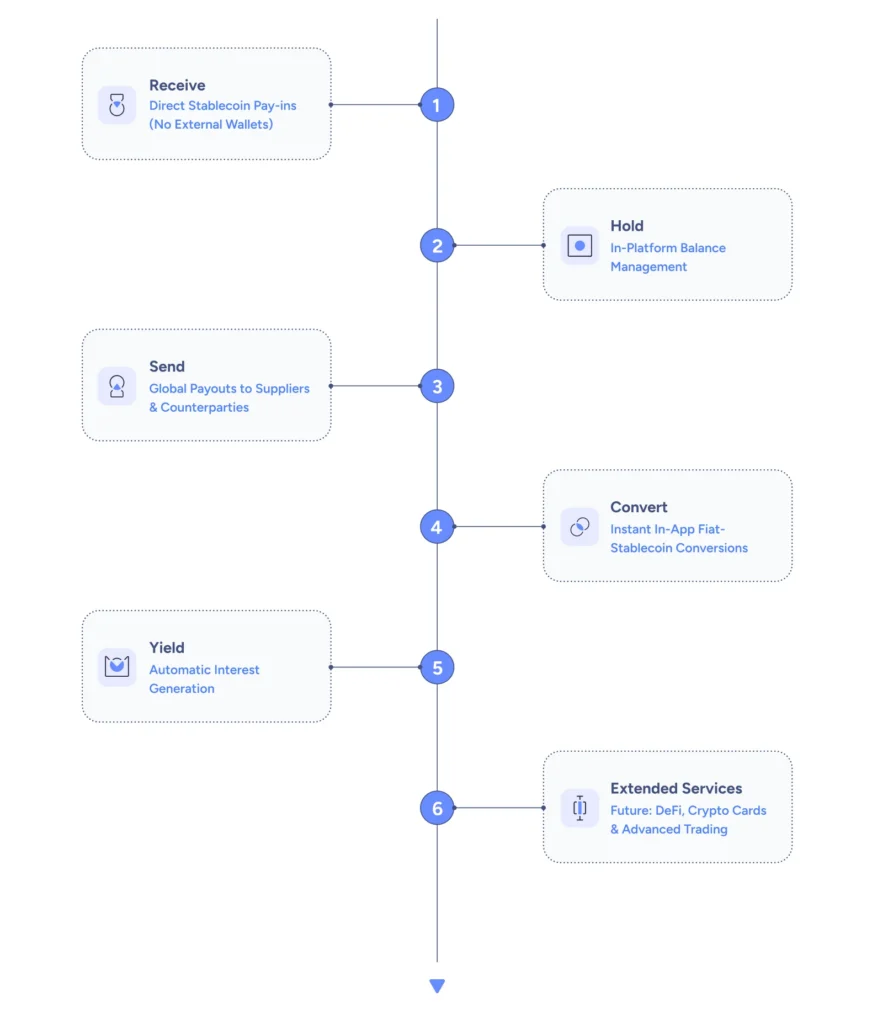

Step 3: Enable In-Platform Transactions and Services

With embedded wallets live and governed, enable the transaction flows that keep user activity on-platform. The infrastructure handles compliance and reconciliation for each of these flows. Nothing new needs to be built at the compliance or settlement layer.

Step 4: Wallet-Level Reconciliation

Each embedded wallet reconciles in real time using the same infrastructure that governs your pay-in and pay-out flows. Blockchain transaction data is normalized, validated, and enriched before it enters your ERP or accounting systems. The output format is MT94x, BAI2, or whatever your existing financial systems already ingest.

Every transaction, balance change, yield accrual, and conversion in every embedded wallet is captured in an immutable onchain record and surfaced through your reporting infrastructure. Real-time balance visibility across all active wallets gives your operations team a live view of the funds held in-platform at any moment.

For PSPs: merchant-level financial reporting in your platform dashboard. Every merchant sees their own balance, transaction history, and yield accruals. Your operations team sees the aggregate view across all merchants.

For B2B providers: client-level reporting with AR and AP matching. Wallet transactions map to invoices and obligations automatically, giving your clients a complete picture of their stablecoin treasury position alongside their payment flows.

Step 5: Roll Out and Monetize

Start with the users who are already active on your pay-in and pay-out infrastructure. They’re the highest-value conversion target because the workflow change is minimal: instead of routing to an external wallet after a payment settles, they hold and manage that balance in-platform. For these users, the embedded wallet is the natural next step, not a net-new product.

From there, expand the embedded wallet offer to your broader user base as a platform feature included with account setup. The onboarding friction is low. Wallet creation is invisible, authentication uses passkeys, and the user experience mirrors a standard fintech account.

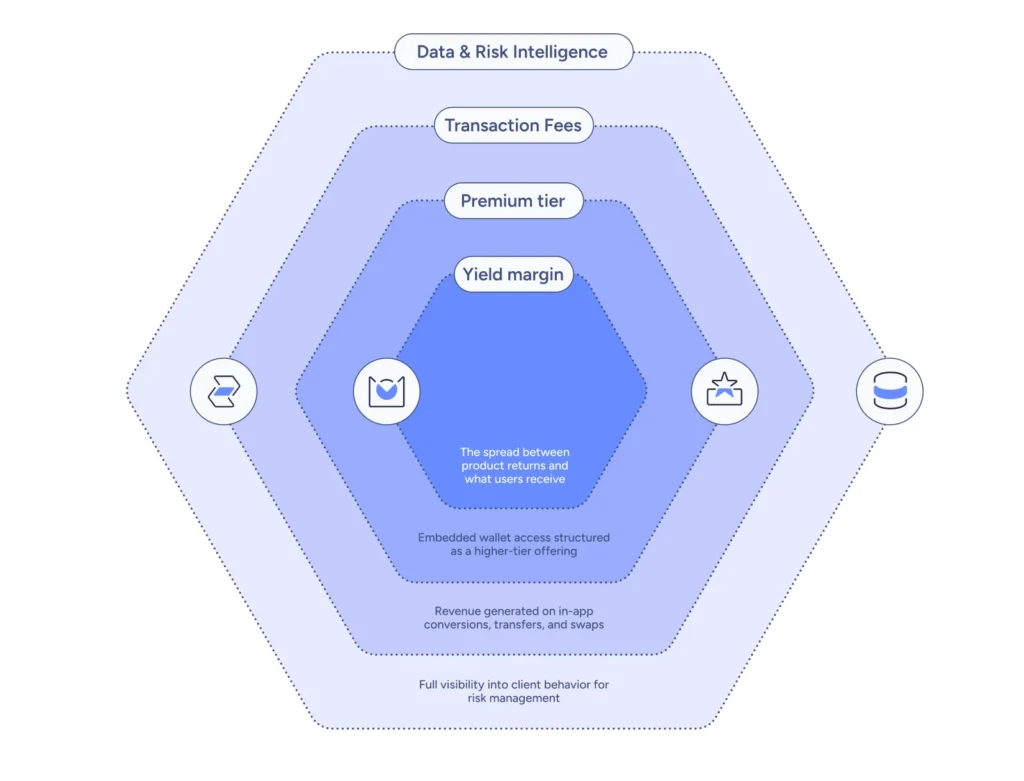

The monetization model has four distinct layers:

What You’ve Built

Every merchant and business client now has a wallet inside your platform, and every financial activity that was previously happening externally happens inside your ecosystem.

Money flows in through pay-ins. It’s held, managed, and put to work through user accounts. It flows out through payouts. The entire cycle runs within your UX, governed by enterprise-grade policy enforcement, and reconciled in real time by infrastructure that outputs into the financial systems your team already operates.

Treasury optimization reduces your operational costs. Pay-in and pay-out infrastructure expands your geographic reach and removes corridor friction. User accounts deepen customer relationships and open revenue streams that none of the previous layers could access on their own. Together, they convert a cross-border payment infrastructure into a stablecoin financial platform.

The practical outcomes across all four layers:

No custody license required. Non-custodial wallet architecture means your merchants and clients hold their own keys. You operate the platform and the experience without taking custody of funds.

Full wallet-level governance. TAP policy enforcement at the wallet level applies to every embedded wallet in your platform. Transaction authorization, velocity limits, asset restrictions, and geographic controls operate consistently across your entire user base.

Sub-second signing speed. MPC architecture delivers real-time wallet interactions for web and mobile. Wallet operations are indistinguishable from standard fintech UX.

Wallet-level reconciliation. Every transaction, balance change, and yield accrual in every embedded wallet reconciles automatically, audit-ready and ERP-integrated.

One platform for all use cases. Treasury operations, pay-ins, pay-outs, and user accounts run on the same infrastructure. No replatforming required as you expand use cases.

Summary: Infrastructure Requirements for Embedded Wallet User Accounts

Running embedded wallets at scale, with governance and reconciliation built in, requires infrastructure built for institutional operations. These are the minimum viable capabilities:

1. Non-custodial embedded wallets. SDKs for web, iOS, and Android with passkey-based authentication, automatic wallet provisioning at account creation, and no seed phrases or private key management surfaced to end users. MPC-based key management and sub-second signing speed handle the security and performance requirements invisibly.

2. Wallet-level policy enforcement. TAP configuration at the individual wallet level, not just at the platform level. Transaction authorization rules, velocity limits, asset restrictions, and geographic controls applied per wallet, with consistent enforcement across your full user base as it scales.

3. Gasless transaction support. Transaction sponsorship that eliminates native token requirements for end users. Reduces operational complexity, removes a category of user support issues, and ensures wallet interactions work regardless of the user’s familiarity with blockchain fee mechanics.

4. In-platform transaction services. Connected Account integrations and Network for Payments access for in-app conversions and transfers. Yield product integrations for idle balance monetization. Batch payout capability connecting embedded wallet outflows to the payout infrastructure from earlier in this series.

5. Wallet-level reconciliation and reporting. Real-time balance tracking and transaction reconciliation across all embedded wallets, with MT94x, BAI2, and ERP-integrated output. Merchant-level and client-level reporting that maps wallet transactions to invoices and obligations. Audit-ready onchain records for every wallet operation.

6. Scalable provisioning. Programmatic wallet creation via API, with no manual setup per user. The same security model and governance framework that applies to a pilot cohort of wallets should operate identically across tens of thousands of active wallets in production.

7. Compliance continuity across wallet operations. AML screening, sanctions checks, and Travel Rule compliance running on every transaction from every embedded wallet, using the same integrations with Chainalysis, Elliptic, Notabene, and GTR that govern your pay-in and pay-out flows.

Completing the Blueprint

User accounts are the final layer of a stablecoin payments platform built for long-term competitive advantage. The payment providers who build this infrastructure now are converting operational efficiency gains from the first three blueprints into durable customer relationships that compound over time.

To discuss how embedded wallet infrastructure applies to your specific platform architecture, user base, and revenue model, speak with a Fireblocks payments specialist or explore how customers including Western Union and Bitso are powering user accounts with Fireblocks and Dynamic today.