Most banks approach digital assets with the same assumptions they use for traditional custody. It is a natural starting point, but it does not hold. Digital assets behave differently, and control that once sat inside core systems now has to be applied in the wallet layer. Institutions that understand this now gain meaningful advantages in speed, flexibility, and market positioning.

To set a future-proof operating model, every institution must answer two questions:

- How much control is required over the assets themselves? This decision defines the custody model. It determines who can move assets, how approvals work, and how operational and supervisory risks are managed.

- What level of connectivity is needed to operate across onchain networks? This determines where the institution can participate, how value moves across networks, and how internal systems link to the broader digital asset ecosystem.

Together, these choices shape the wallet infrastructure the institution deploys. The wallet layer is where control and connectivity are implemented. It governs how assets are secured, how transactions are approved, and how policies are enforced across all digital asset workflows.

Seen this way, digital asset custody is not a downstream operational task. It becomes a strategic foundation. The custody model a bank adopts sets the boundaries for what it can operate directly, how quickly it can launch products, and how confidently it can scale services in markets that operate continuously.

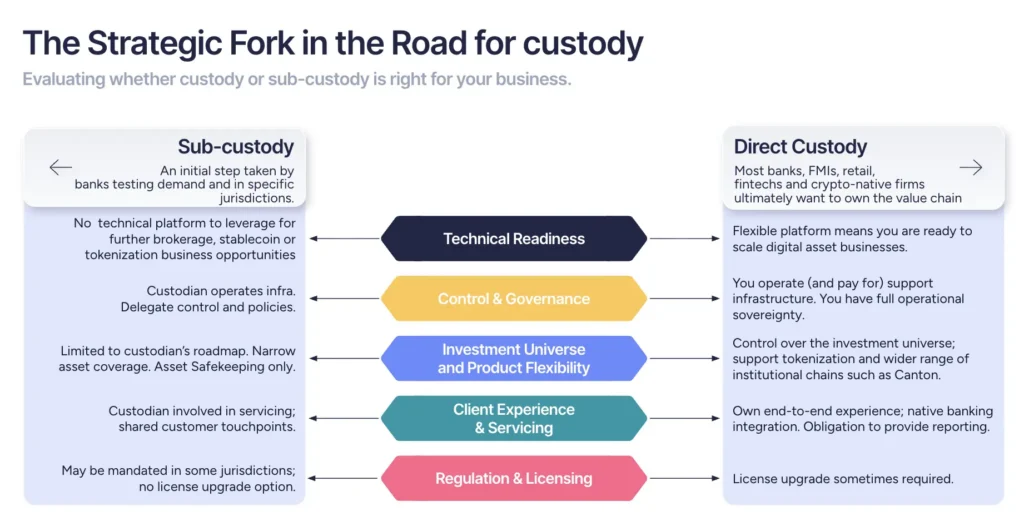

Direct vs. Sub-Custody: The Strategic Fork in the Road

As banks define their digital asset strategies, they face a critical structural decision: whether to choose direct custody capabilities or rely on a third-party custodian. This choice determines operational control, competitive positioning, and revenue potential across all digital asset services.

Direct custody gives the bank operational sovereignty by keeping control over how assets move and how onchain actions are executed inside its own perimeter rather than relying on a third-party custodian. While using a sub-custodian can mean faster time to market, it does introduce structural constraints on speed, risk management, and product design.

Leading institutions recognize these constraints and choose direct custody to ensure strategic control. This approach enables banks to respond immediately to client needs, access optimal liquidity venues, and align custody operations with supervisory expectations and internal governance standards

For banks, direct custody becomes the foundation that enables scalable, relevant service offerings in the digital asset economy.

The timing of this infrastructure decision determines a bank’s competitive positioning in digital finance for the next decade.

What Direct Custody Delivers

Banks cannot deliver modern digital asset services by adapting legacy systems. Traditional infrastructure lacks the cryptographic controls, real-time enforcement, and blockchain connectivity that these services require. It’s not how onchain finance works

Direct custody removes those limitations. It provides the operational control layer that enables institutions to launch, scale, and govern digital asset services with confidence. This control covers both transaction signing for asset movement and the administration of smart contracts that automate onchain actions.

Its strategic value comes into focus across four core areas:

- Transaction-intent integrity

Banks need end-to-end assurance that what a user thinks they are signing matches what the wallet signs and what ultimately executes onchain. This is the essential safeguard against unintended actions and a core element of operational risk management. - Continuous operations and market-speed execution

Direct custody gives banks the ability to operate on new terms, executing transactions, settling trades, and supporting clients 24/7. Services like trading, staking, and cross-border payments become possible without being constrained by sub-custodian hours, batch processing windows, or manual interventions. And in the current market, banks face competition with crypto-native firms, who are used to 24/7 digital asset markets. - Drives competitive advantage

Owning the custody layer allows banks to move on their own terms, without outsourcing revenue, security, compliance, or risk. It also gives them the agility to drive new business: banks can start with a single service, such as stablecoin issuance or institutional safekeeping, and expand into adjacent offerings as strategy and demand evolve. - Compliance alignment and future-proofing

Custody defines how governance, control, and compliance are operationalized. With direct access to policies, permissions, and audit trails, banks can meet supervisory expectations while maintaining flexibility to adapt as regulatory frameworks evolve globally. It also carries the day-to-day control functions that banks rely on, such as segregation of duties, entitlements, attribution, non-repudiation, and policy checks that coordinate approvals across teams.

These capabilities do more than support digital asset strategy. They define how institutions grow, govern, and compete in a market that rewards speed, transparency, and control. Once this control layer is established, banks can build and scale the services that matter most to clients.

Custody as the Gateway to Comprehensive Digital Asset Services

Custody serves as the operational foundation that enables banks to build and scale digital asset services across four key business lines, regardless of which products they prioritize or how their strategy evolves. This foundational approach allows institutions to choose their entry point based on strategic priorities while building the infrastructure capabilities that support multiple use cases simultaneously as market opportunities develop and internal capabilities mature.

Stablecoin Banking and Payments

Whether serving retail or institutional clients, banks that issue or accept stablecoins must enforce policy controls, manage key security, and support regulatory reporting across jurisdictions. Custody infrastructure is what enables this.

Whether serving retail users or corporates, stablecoin flows demand secure key management, programmable controls, and full auditability. The Wenia platform enables 24/7 programmable payments via its fiat-backed stablecoin, $COPW, giving users round-the-clock access to funds beyond traditional clearing hours. Oddo BHF provides similar functionality for corporates and institutional clients through its euro stablecoin, EUROD. In both cases, custody provides the underlying control layer for issuing, managing, and enforcing stablecoin operations at scale.

Client-Facing Digital Asset Custody Services

BNY built its Digital Assets Platform to serve institutional clients with production-scale infrastructure. The platform combines flexible key management, automated approval policies, and audit-ready controls. This architecture enables banks to offer services like safekeeping, collateral management, and staking, turning traditional custody into a scalable, revenue-generating business line for new markets.

Trading and Brokerage

Direct custody allows banks to offer trading services without compromising asset protection or regulatory oversight. By separating custody from execution, institutions reduce counterparty risk while maintaining access to liquidity across exchanges, OTC desks, and market makers. Policy controls embedded at the custody layer enforce trading permissions, monitor exposure in real time, and enable instant settlement, without relying on traditional clearing timelines.

Sygnum’s instant settlement network demonstrates this approach in practice, connecting over 200 institutional clients for 24/7 movement of fiat and digital assets.

Token Lifecycle Management

In 2023, Siemens showed what’s now possible in capital markets: a fully-regulated digital bond issued under the German Electronic Securities Act and settled entirely onchain. All was done without touching an FMI.

To operate at this level, banks need control from issuance through redemption. Smart contracts must be deployed securely, transfer restrictions enforced automatically, and asset servicing aligned with securities regulations. With the right custody architecture in place, banks can govern every stage while keeping assets liquid and operations compliant.

Custody also supports reconciliation and reporting, linking internal books to blockchain activity and providing the audit trails, proofs of control, and regulatory reporting banks depend on.

Tokenization is increasingly the context in which banks first encounter custody questions that are embedded in product decisions. The Exec Tokenization Reading List covers what boards and product leaders need to understand before building.

Custody Is the Control Layer for Digital Assets

Digital asset custody is done differently. It defines how assets move, how risks are controlled, and how services scale in a market that operates in real time. There are no clawbacks on a blockchain.

It is the foundation for stablecoin payments, institutional custody, tokenized markets, and onchain treasury. It is the operational layer that gives banks the ability to deliver secure, compliant services with confidence.

The SEC’s September 2025 no-action letter shifted the conversation on what “proper custody” requires for digital assets. This piece covers what that guidance means operationally for institutions holding customer assets.

The decisions banks make about custody today will determine how they grow, compete, and lead in tomorrow’s digital economy. The digital assets space is dynamic and fast-changing. Join the more than 80 banks around the world who are already working with Fireblocks to build their next-generation custody stack, while the opportunity to lead is still open.

FAQ

-

What security standards should banks expect from digital asset custody infrastructure?

Banks should expect custody infrastructure that supports both MPC (Multi-Party Computation) and hardware-backed key protection using HSMs or secure enclaves such as Intel SGX. This ensures flexibility to meet internal security standards and regulatory requirements while avoiding single points of failure. They should also expect automated policy engines that enforce institutional-grade approval workflows, auditability, and compliance controls. Banks that require HSM-based key control can use solutions such as Fireblocks Key Link, which lets them keep keys inside their own HSMs while using Fireblocks for governance and operations. -

How do banks demonstrate digital asset custody compliance to regulators?

Banks must implement infrastructure that supports DORA, Basel, and MiCA alignment with built-in examination readiness protocols. This includes real-time controls like sanctions screening, transaction monitoring, Travel Rule compliance, and comprehensive audit trails that demonstrate operational resilience and risk management capabilities. -

What operational risks should banks consider when evaluating custody models?

Direct custody provides operational control and 24/7 capabilities but requires internal expertise and infrastructure investment. Sub-custody can be an initial approach, but can introduce counterparty risk, timing restrictions, and dependency on external roadmaps that can limit strategic flexibility and competitive positioning. -

How does digital asset custody generate revenue for banks?

Custody infrastructure enables multiple fee-generating services including safekeeping, collateral management, staking services, trading facilitation, stablecoin banking, and tokenized asset management. It serves as the operational foundation that determines what digital asset business lines banks can offer and scale. -

How do banks choose between custody infrastructure providers?

Banks should evaluate providers based on regulatory compliance capabilities, security architecture (MPC vs. traditional methods), ecosystem connectivity, integration complexity with existing systems, and proven track record with regulated financial institutions