Introduction: How Stablecoins Change the B2B Cross-Border Payments Landscape

You’ve already optimized your corporate treasury with stablecoins. Settlement is faster, capital is cycling more efficiently, and your internal operations are running on rails that weren’t possible two years ago. Now comes the harder question: how do you extend those same capabilities to the actual payment flows that drive your revenue?

B2B cross-border payments are where the structural inefficiencies of traditional banking have the most visible business impact. If you’re operating payment flows for enterprise clients, you’re managing the consequences every day. Corridor liquidity gets trapped in prefunded accounts waiting for multi-day wire settlement. Every new geography means a new correspondent banking relationship, new fees, new float requirements. Reconciliation across those corridors is manual, error-prone, and a constant source of friction for your finance team. Your clients’ suppliers sit in markets where reliable banking access is limited, and getting them paid requires workarounds that slow everything down and cost margin at every step.

Stablecoin infrastructure addresses each of those problems at the operational level with structural change to how payment flows are built. This blueprint provides a step-by-step implementation guide for B2B payment providers building stablecoin pay-out and pay-in infrastructure: the mechanics of how to construct the flows, how to connect to liquidity, how to handle compliance across corridors, and how to reconcile everything in a format your finance team already understands.

This blueprint provides a practical, step-by-step implementation guide for transforming your pay-in and pay-out operations globally.

Use Case 1: Pay-Outs: Cross-Border Disbursements That Free Trapped Liquidity

The Problem

Every cross-border disbursement corridor you operate has the same underlying problem: capital tied up waiting for settlement to clear. Wire transfers take days. Correspondent banking fees eat margin on every transaction. Opening a new corridor requires establishing a new banking relationship, and then funding it. The more corridors you run, the more capital you’re tying up in prefunding.

The net effect is a business model where your operational cost scales linearly with your geographic ambition. That’s the constraint stablecoin pay-outs remove.

With stablecoin infrastructure, disbursements settle at T+0 in any corridor. Recipients can receive funds into stablecoin wallets without a bank account on their end, which changes what’s possible in emerging market corridors entirely. And because settlement is instant, the prefunding logic that governs your current operations changes: capital cycles faster and ties up less. Conduit, a B2B payments company operating across LatAm and Africa, freed 100% more liquidity in one month after switching to stablecoin rails via Fireblocks, and opened new corridors on the same platform without adding new vendors.

A Step-by-Step Operational Blueprint for Stablecoin Pay-Outs

Step 1: Extend Your Vault Architecture for Payout Flows

The vault structure you built in Part 1 is the starting point. Extend it with a payout-specific layer: a central treasury vault that feeds into corridor-specific payout vaults.

For payout operations at scale, the key architectural decision is how many withdrawal vault accounts to run and how to distribute load across them. The right approach is multiple withdrawal vault accounts with round-robin routing, distributing withdrawal requests across wallets in a circular execution pattern to reduce queue risk and increase throughput.

Step 2: Configure Your Policy Engine

Once vault structure is set, configure your Policy Engine for payout-specific governance:

- Multi-level approval thresholds calibrated to your B2B transaction sizes

- Velocity limits per corridor and per client

- Maximum exposure limits per counterparty

The Policy Engine is where your business controls live. Build it to match the governance logic you already apply to traditional payment operations. The infrastructure should enforce your rules automatically, not require manual oversight at every step.

Step 3: Define How Your Payout Vaults Get Funded

Before execution flows can run, you need a funding model. The two primary approaches are pre-funding and Delivery versus Payment (DvP), and the right choice depends on your account structure and corridor architecture.

With pre-funding, you convert fiat to stablecoin in advance and hold liquidity, ready to sweep into the relevant vault as disbursements are triggered. This is the simpler operational model and works well when you have predictable corridor volumes and want to minimize settlement latency.

DvP links funding and disbursement atomically: funds move only when the corresponding obligation is confirmed. This reduces the capital tied up in pre-funded positions but requires tighter integration between your funding source and payout execution layer.

Your account structure also shapes the funding model. An omnibus vault consolidates float, which simplifies the funding mechanics but requires clean sub-ledger logic to maintain fund separation. A segregated structure means each client account is funded independently, either directly from the client or swept from your central treasury at the point of disbursement. For B2B operations, where client-level audit trail matters, segregated funding flows are typically the cleaner operational choice.

If your corridors involve cross-chain settlement, funding also needs to account for the bridging step: stablecoin on one chain may need to be converted or bridged before it reaches the destination vault. Build this into your funding logic at configuration.

Step 4: Connect to Liquidity and Access Multiple Providers

Before you build the payout flow, map your highest-cost corridors. Prioritize where correspondent banking fees, FX spreads, and float costs are currently largest. Those are the flows where stablecoin infrastructure delivers the most immediate margin improvement.

Then connect to liquidity providers through the Fireblocks Network for Payments. A single API integration gives you access to 2,400+ institutional counterparties across 60+ currencies and 100+ countries, with the ability to route each corridor to the best-priced provider at the moment of settlement. That multi-provider access is the structural differentiator for B2B operations.

Single-provider dependency is a real operational risk in B2B payments: if your liquidity provider has pricing power over your corridor, has downtime, or has coverage gaps in markets you’re expanding into, you’re stuck. Multi-provider access through the Network eliminates that dependency. Arf improved liquidity 100% in one month specifically because multi-provider access via the Network gave them routing flexibility they couldn’t get from a single-provider arrangement.

Establish redundancy at this stage: define fallback routing so that if one provider has unfavorable rates or downtime on a specific corridor, traffic routes automatically to the next option. Build this logic into your configuration before you go live.

Step 5: Build the Cross-Border Payout Flow

With vault structure and liquidity connections in place, build the payout execution layer using automated workflows.

Configure payment flow templates that embed compliance, liquidity routing, and reconciliation into the execution logic itself, not as steps that happen after the fact. Then define your payout triggers:

- Event-driven: invoice approved triggers automatic disbursement

- Scheduled: batch payouts at defined intervals for specific corridors or client accounts

Route each corridor to the best-priced provider via a global payments network. The routing logic should run automatically; your operations team shouldn’t be making per-transaction provider decisions.

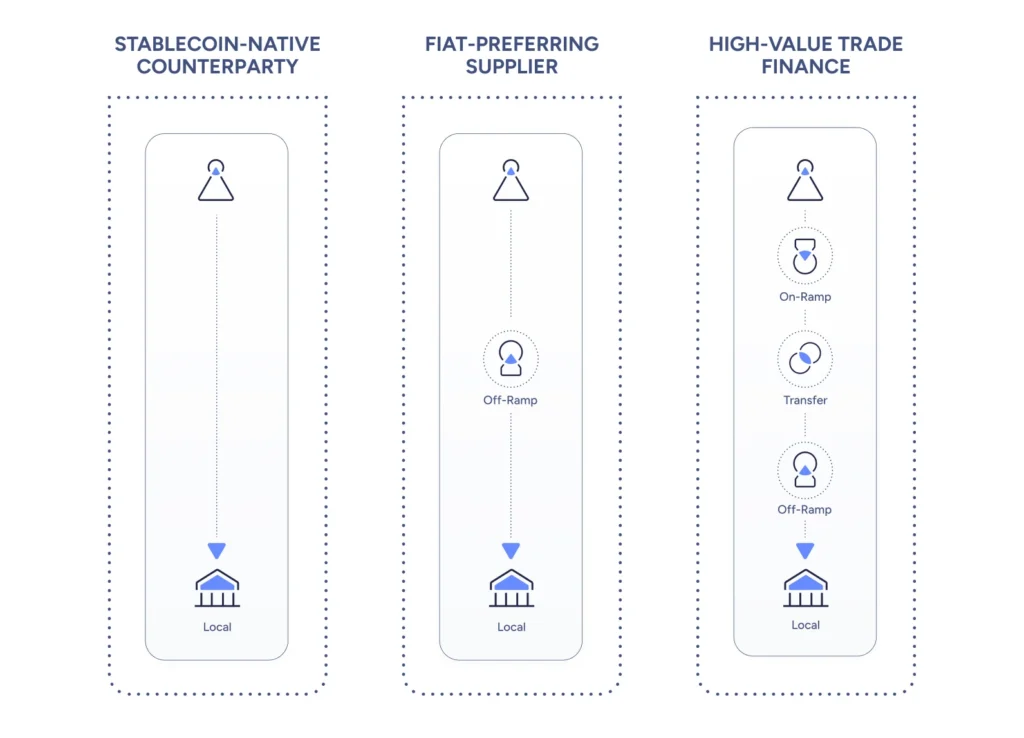

The practical payout paths vary by recipient type:

Take the example of a LATAM-based client with a ship waiting outside Singapore to refuel. A payment flow that would traditionally take a week through correspondent banking becomes a same-day transaction on stablecoin rails. The operational leverage of that change is measurable for every client whose business requires time-sensitive cross-border disbursements.

Step 6: Configure Payout Compliance

For B2B payment operations across multiple jurisdictions, compliance can’t function as middleware bolted onto the side of your payment flow. It needs to be embedded in every transaction before execution.

Integrations with Chainalysis, Elliptic, Notabene, and GTR handle AML screening, sanctions checks, and Travel Rule compliance across the full transaction lifecycle. Auto Freeze holds flagged transactions for review before they execute. A Policy Engine applies compliance rules at the corridor, client, and transaction-size level, keeping your compliance posture consistent across all flows without requiring manual configuration for every new transaction.

B2B compliance has specific complexity that consumer payment flows don’t: multi-jurisdiction screening, KYB requirements for business counterparties, and beneficial ownership structures that may involve multiple entities across different regulatory regimes. Build your compliance configuration to handle those requirements explicitly, rather than treating B2B transactions as scaled-up consumer flows.

Step 7: Payout Reconciliation

The operational gains from stablecoin settlement only fully materialize if reconciliation keeps pace. For B2B operations, that means enterprise-grade reporting in formats your finance team already works with.

An infrastructure provider should deliver MT94x and BAI2 reconciliation reports with full ERP integration. Blockchain transaction data is normalized, validated, and enriched before it enters your accounting systems. Finance teams work with familiar statement formats rather than raw onchain data. Deterministic onchain confirmations replace the ambiguity of matching across correspondent banks with different systems and different batching schedules.

At the operational level, your team gains real-time visibility into all in-flight disbursements across corridors. Client-level reporting shows disbursements by status: pending, settled, flagged. Payout data flows directly into AP matching, invoice reconciliation, and corridor-level P&L reporting via your ERP integration. The reconciliation overhead that currently scales with corridor volume doesn’t scale the same way when the underlying transaction record is deterministic and automated.

Use Case 2: Pay-Ins: Receive B2B Payments Faster, Reconcile Automatically

The Problem

Receiving payments from business clients via wire transfer creates a specific set of operational problems that reconciliation workarounds don’t actually solve. Payments arrive with ambiguous status. AR matching requires manual effort to connect incoming transactions to the right invoice and client. For clients in emerging markets, banking access adds another layer of friction. And chargeback exposure, while less acute for B2B than consumer flows, is an added complexity that stablecoin settlement eliminates entirely.

The stablecoin pay-in model changes the AR dynamic fundamentally. Onchain confirmation is deterministic: there is no ambiguity about whether a payment was sent or received. Automated AR matching becomes possible because each incoming transaction can be mapped to a specific invoice and client with certainty. Clients in markets with limited banking access can pay via stablecoin without a bank account on their end. And once funds arrive, there’s no reversal risk.

Step 6: Design Your Pay-In Account Structure

Extend your vault hierarchy with receiving accounts built for B2B inbound flows. The account structure should follow the same segregated logic that governs your payout layer: each business client gets a dedicated deposit address, with per-client or per-invoice addressing that enables automated reconciliation downstream.

For B2B pay-ins, segregated accounts do more than simplify reconciliation. They create clean fund separation that maps each incoming payment to a specific client and obligation from the moment funds arrive. This matters for your audit trail, your client reporting, and your compliance posture.

Step 7: Build the Inbound Payment Flow

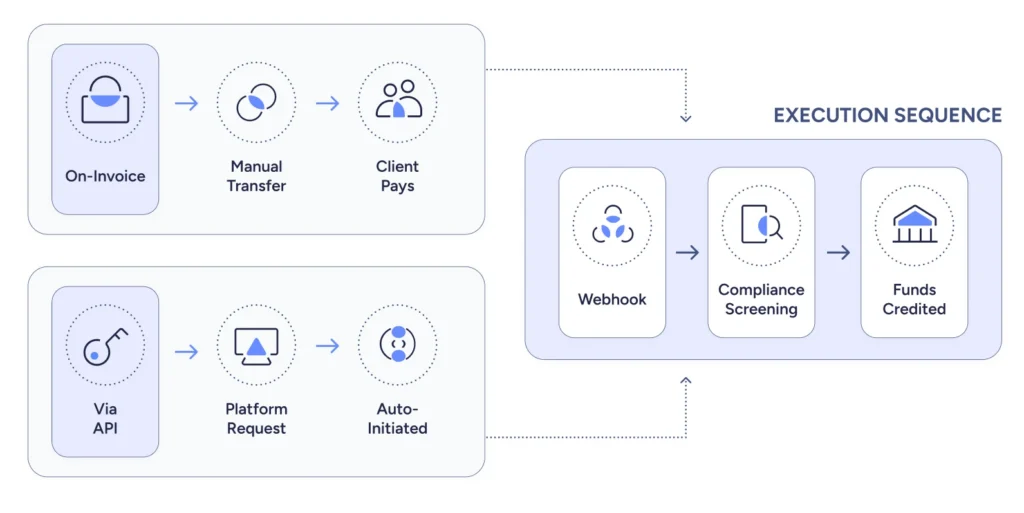

Once account structure is configured, the inbound flow works at three points of integration:

- On invoice: the client’s invoice includes a stablecoin deposit address alongside traditional payment instructions. They pay by sending stablecoin to that address.

- Via API: integrate the pay-in address generation into your platform so clients can initiate stablecoin payments programmatically, without any manual address communication.

- The execution sequence: client sends stablecoin → confirmed via webhook → compliance screening → payment credited to the segregated client account.

The practical pay-in paths for B2B operations include:

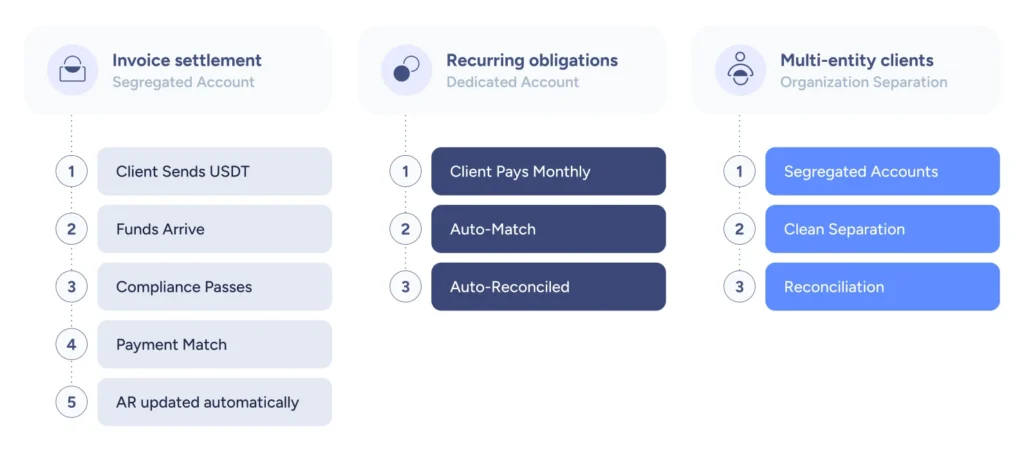

- Invoice settlement: client sends USDT to pay an invoice; funds arrive in the segregated account, compliance passes, the payment matches to the open invoice, AR is updated automatically.

- Recurring obligations: client pays monthly amounts to a dedicated address; each transaction is auto-matched and auto-reconciled without manual intervention.

- Multi-entity clients: different client entities pay into different segregated accounts, giving you clean separation for reconciliation across complex organizational structures.

Step 8: Inbound Compliance Screening

Screen source wallets before crediting, not after. Chainalysis and Elliptic integrations handle risk scoring on incoming transactions. Travel Rule requirements (originator and beneficiary information shared between Virtual Asset Service Providers) are handled at the transaction layer for stablecoin transfers.

For new payer wallets, your KYB onboarding framework should require sender address registration and verification before the first pay-in is processed. Auto Freeze holds flagged payments for manual review. Policy Engine configuration governs which stablecoins are accepted, transaction thresholds, and whether clean-screened sources auto-approve or route to manual queue.

Compliance screening on inbound flows is often treated as a lighter-weight process than outbound, because the funds are arriving rather than leaving. For B2B operations at scale, that is a mistake. Source wallet screening on high-value inbound transactions is operationally and regulatorily important. Build it as a mandatory step in every pay-in flow, not an optional flag.

Step 9: Post-Receipt Processing and Netting

After pay-in funds clear screening, configure automated sweeps from client segregated accounts to your central treasury. Convert to fiat using the same off-ramp infrastructure from the payout layer if needed.

The payment matching logic runs automatically: incoming amount plus sender wallet maps to an open invoice, marks it as paid, and triggers downstream AP/AR workflows without human intervention. Configure thresholds for straight-through processing vs. manual queue so your AR team is handling exceptions, not routine matches.

Net settlement is where the two-way flow creates operational efficiency. Stablecoins received as pay-ins offset outbound payouts, reducing the number of on/off-ramp cycles required and lowering conversion costs across the full flow. For clients who maintain recurring relationships, you can offer balance optionality: hold stablecoin balance, off-ramp to fiat, or apply directly to future obligations. This flexibility has real value for enterprise clients managing treasury across multiple corridors.

Step 10: Pay-In Reconciliation

Every incoming payment reconciles in real time. The same MT94x, BAI2, and ERP integration that governs your payout reconciliation applies to inbound flows. Blockchain transaction data is validated, normalized, and enriched before entering your ERP, so finance teams see clean, familiar statement formats, not raw onchain data.

Invoice-level reconciliation maps each pay-in to a specific invoice with automated status updates in your billing system. AR matching is automated rather than manual, which changes the operational load of your finance team significantly as payment volumes scale. The complete audit trail for every inbound payment is immutable and available onchain, which simplifies audit processes considerably compared to reconciling across correspondent banking systems.

What You’ve Built

Completing the steps in this blueprint gives you a two-way cross-border payment engine. Business clients pay invoices in stablecoins with automated AR matching, and you pay their suppliers and counterparties with instant disbursements across corridors and multi-provider liquidity routing. Trapped corridor liquidity is freed. Correspondent banking dependencies are bypassed. Every transaction, inbound and outbound, reconciles in real time in a format your existing financial systems already handle.

The practical results of this build map directly to the business metrics that matter:

Settlement speed. T+0 disbursements replace multi-day wire settlement across every corridor. Bridge (now part of Stripe) reduced bulk settlement time from over 12 hours to under 90 minutes using Fireblocks infrastructure.

Liquidity efficiency. Instant settlement reduces prefunding requirements across corridors. Arf improved liquidity 100% in one month by gaining multi-provider access via the Fireblocks Network for Payments.

Geographic reach. The Fireblocks Network for Payments connects you to 2,400+ institutional counterparties across 60+ currencies and 100+ countries. New corridors open via network connectivity, not new banking relationships. Conduit opened new corridors across LatAm and Africa on the same platform, with no new vendors required.

Reconciliation automation. MT94x, BAI2, ERP-integrated, audit-ready reconciliation across all pay-in and pay-out flows. Blockchain data validated and normalized before it reaches your finance team.

Recipient flexibility. Pay out to stablecoin wallets without a bank account on the recipient side. Transformative for emerging market corridors where banking access is inconsistent.

Security at scale. $10T+ in digital asset transactions secured, zero breaches, and up to $360M per-customer insurance.

The infrastructure doesn’t require you to rebuild as your use case expands. Triple-A started with payments and expanded to Wallets-as-a-Service and treasury management on the same Fireblocks platform, with no replatforming required. The same foundation that powers the pay-in and pay-out flows in this blueprint supports user account infrastructure and further treasury automation as your stablecoin strategy matures.

Summary: Infrastructure Requirements for B2B Stablecoin Pay-In and Pay-Out Operations

Building two-way stablecoin payment flows at B2B scale requires infrastructure built for institutional operations. The following capabilities are the minimum viable foundation:

1. Flexible vault architecture with segregated account support. Structure wallets and payment accounts to reflect your operational reality: corridor-specific vaults, client-level segregation, and hierarchical controls that match your treasury governance model. For B2B operations, segregated accounts are the right default: they create the audit trail and fund separation that high-value enterprise transactions require.

2. Multi-provider liquidity access with no single-provider lock-in. Corridor routing that lets you optimize for cost, reliability, and coverage simultaneously. Single-provider dependency is an operational and commercial risk. Multi-provider access via a pre-integrated network removes it. The Fireblocks Network for Payments provides access to 2,400+ institutional counterparties across 60+ currencies.

3. Automated payment flow execution with embedded compliance. Payment flow templates that embed AML screening, Travel Rule compliance, and sanctions checks into transaction execution, not as bolted-on middleware. They are part of the flow itself. Integrations with Chainalysis, Elliptic, Notabene, and GTR, with Auto Freeze for flagged transactions and a Policy Engine that applies configurable rules per corridor, client, and transaction size.

4. Enterprise-grade reconciliation and ERP integration. MT94x and BAI2 reports with full ERP integration, automated across all pay-in and pay-out flows. Invoice-level AR matching, corridor-level P&L reporting, and real-time visibility into all in-flight transactions. Blockchain data normalized and enriched before it reaches your accounting systems.

5. Deterministic settlement and audit trail. Onchain confirmation eliminates the reconciliation ambiguity that comes from matching records across correspondent banks with different systems and different timing. Every transaction, inbound and outbound, has an immutable, complete audit trail.

6. Recipient wallet flexibility. The ability to disburse to stablecoin wallets without requiring a bank account on the recipient side. This is the operational requirement that opens emerging market corridors that are currently closed to your business due to banking infrastructure gaps.

7. Scalable platform with no replatforming requirement. Infrastructure that handles pilot volumes and production volumes on the same architecture. As your stablecoin payment operations grow from initial corridors to company-wide infrastructure, the security model, policy rules, and operational workflows should scale without fundamental changes.

Next Steps

The pay-in and pay-out infrastructure you’ve built in this blueprint is the foundation for a complete stablecoin payments platform. The final part of this series will cover building client-facing stablecoin accounts, extending the same infrastructure to the user account layer and opening the additional revenue streams and client relationships that come with it.

If you’re ready to discuss how this architecture applies to your specific corridors, volumes, and client base, speak with a Fireblocks payments specialist or see how payments customers like Checkout.com, Euronet, and Conduit are building on Fireblocks today.