Introduction: The PSP Payment Flow Today

Traditional PSPs sit at the center of a deceptively complex chain. On one side, you’re accepting payments from consumers through card networks, bank transfers, and local payment methods. On the other, you’re settling those funds with merchants, often across borders, always subject to banking hours, and invariably slower than either party would like. Between those two endpoints, capital moves through a sequence of intermediaries that each add cost, time, and reconciliation burden.

You’ve already optimized your treasury operations with stablecoin infrastructure, so you have the foundation in place: wallet architecture, liquidity connections, compliance controls, automation rules, and reconciliation. This blueprint extends that foundation to the two payment flows that define your business: accepting payments from consumers (pay-ins) and settling funds with merchants (merchant settlement).

These are the flows where stablecoins create the most visible competitive advantage for a PSP. Pay-ins determine how much margin you retain on every transaction, and how much choice you provide to consumers. Merchant settlement determines how fast your merchants get paid and, increasingly, whether they stay with you or move to a competitor offering instant settlement. Together, they represent the core of your value proposition to merchants: accept more payments efficiently, settle quickly.

Leading PSPs are already live on stablecoin settlement rails. Competitors shipping instant settlement are winning merchant relationships while PSPs in “evaluation mode” are falling behind. Here’s your practical, step-by-step implementation guide for accepting stablecoin payments and settling with merchants on stablecoin rails.

Use Case 1: Stablecoin Pay-Ins

What you’re solving

Card processing fees of 2-3% per transaction eat directly into your margin or your merchant’s margin, depending on your pricing model. Chargebacks cost money and operational overhead on every disputed transaction. And expanding to new geographies means integrating with local acquiring banks and local payment methods, each requiring significant technical resources. Stablecoin pay-ins address all three simultaneously. When you have the infrastructure to accept stablecoins, you can start retaining more margin.

The stablecoin advantage

Stablecoin pay-ins introduce a fundamentally different acceptance model:

- More options for consumers to pay. As stablecoin adoption grows, consumers and business buyers want the option to pay with digital assets. Offering stablecoin acceptance at checkout meets demand that card-only PSPs can’t serve.

- Higher margin retention. Stablecoin acceptance costs approximately 0.5% per transaction, compared to 2-3% for card processing. For a PSP processing billions in annual volume, that margin difference is substantial. You’re not just saving on fees, you’re retaining revenue that was previously distributed across card networks, scheme operators, and acquiring banks.

- Zero chargeback risk. Blockchain transactions are final. Once a stablecoin payment is confirmed onchain, it cannot be reversed. There are no chargebacks, no friendly fraud disputes, no chargeback processing overhead, and no chargeback ratio management. This eliminates an entire category of operational cost and risk.

- Geographic expansion with minimal technical overhead. Accepting stablecoin pay-ins in a new market doesn’t require integrating with a local acquiring bank or building local payment method support. The acceptance infrastructure is software-based: a QR code, a wallet address, a checkout integration. Note that while local acquiring bank integrations aren’t needed, local regulatory licensing requirements still apply, but the technical lift to accept payments in a new geography is dramatically reduced.

- T+0 settlement. Funds are confirmed in seconds, not T+2 or T+3 on card rails. This improves working capital for both the PSP and the merchant, and it means you can offer same-day or instant access to settled funds as a product feature.

- Access to underserved merchant segments. Crypto-native businesses, DAOs, web3 companies, and e-commerce merchants serving digital-asset-holding consumers represent a growing segment that is underserved by card-only acceptance. Stablecoin pay-ins let you capture this market without building separate infrastructure.

When looking for a company that provides the intersection of blockchain and payments expertise with an enterprise-grade platform, Fireblocks clearly comes out on top.

nabil manji

SVP & GM – Crypto & Web3, WorldPay

A Step-by-Step Operational Blueprint for Stablecoin Pay-Ins

Step 1: Design Your Pay-In Account Structure

The pay-in infrastructure builds on the vault architecture you deployed in Blueprint 1. You’re extending your existing hierarchy with receiving accounts that are purpose-built for inbound payment flows.

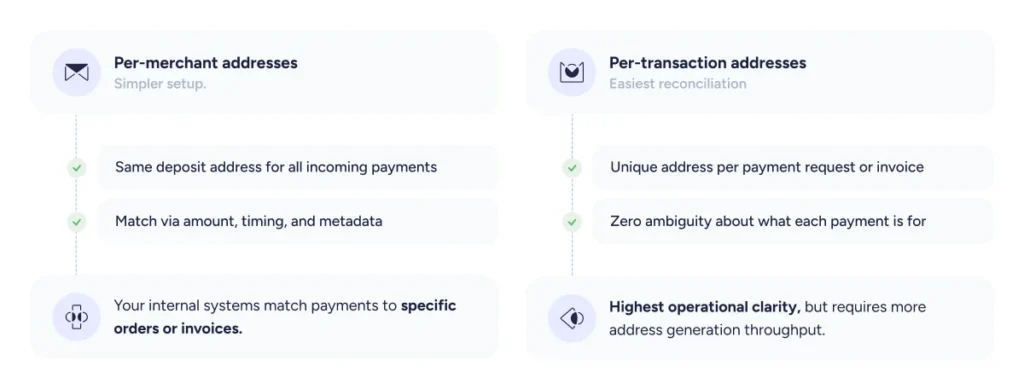

Create segregated deposit accounts per merchant.

Each merchant on your platform gets a unique deposit address with a stablecoin receiving account that maps directly to their merchant account in your system. When a consumer pays to that address, the funds are immediately attributable to the correct merchant without any matching logic or manual reconciliation.

Segregated accounts are strongly recommended for pay-ins. Unlike omnibus structures (which can work well for treasury management), pay-in flows benefit from the clean attribution that segregation provides. Every incoming transaction maps to a specific merchant which simplifies compliance screening, reconciliation, and merchant-level reporting.

Model Selection and Reconciliation Requirements

Choose your addressing model based on your reconciliation requirements:

Configure multi-chain support

Consumers may hold stablecoins on different blockchains, e.g. Ethereum, Solana, Tron, Base, Polygon, and others. Your infrastructure should support receiving on multiple chains so that the payment experience isn’t constrained by which blockchain the consumer uses, meaning you can offer receiving flexibility without managing separate infrastructure per chain.

Step 2: Build the Inbound Payment Flow

With receiving accounts in place, build the flow that moves a consumer’s stablecoin payment from their wallet to your merchant’s account.

Share the deposit address with the payer

How this happens depends on the checkout context:

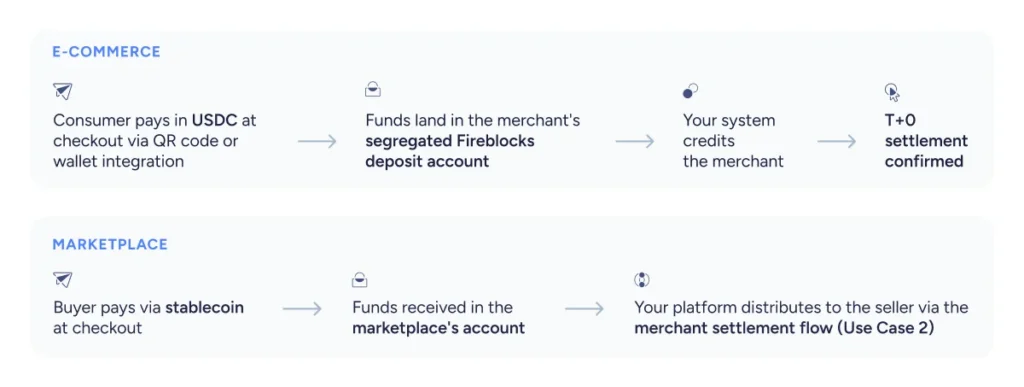

- QR code at point of sale or checkout. The merchant integrates the deposit address as a QR code in their checkout experience. The consumer scans with their wallet app and confirms the payment. This is the model that makes geographic expansion lightweight: deploying stablecoin acceptance in a new market is fundamentally a software integration, not a banking relationship. Note that while the technical lift is minimal, local regulatory and licensing requirements still apply.

- Online checkout integration. The stablecoin payment option appears alongside card and bank transfer at checkout. The consumer selects stablecoin, is presented with the deposit address and amount, and sends the payment from their wallet.

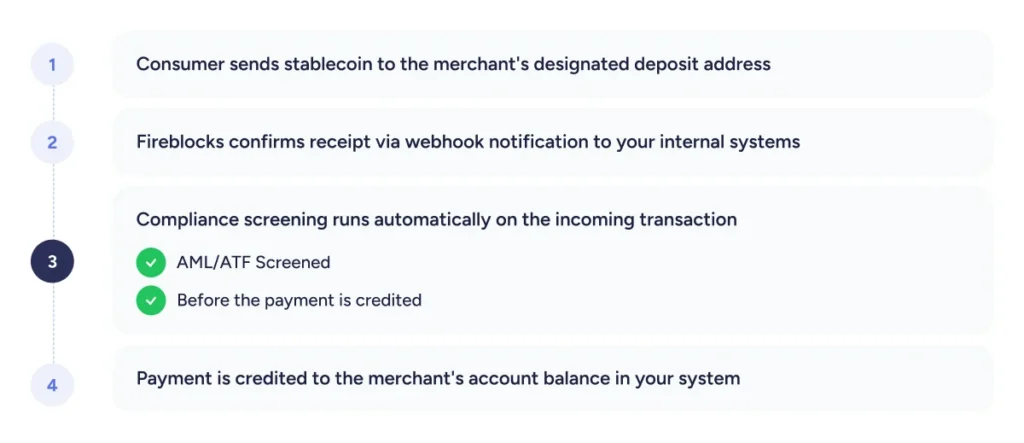

The Payment Flow

The payment flow itself is straightforward:

Example pay-in paths:

Step 3: Inbound Compliance Screening

Pay-in compliance is distinct from outbound compliance. When you’re disbursing funds (merchant settlement), you control both endpoints. When you’re accepting pay-ins, you’re receiving money from external wallets that you don’t control. The compliance burden shifts to screening what’s coming in before you credit the merchant.

Screen incoming transactions before crediting

Configure inbound transaction screening through integrations with Chainalysis, Elliptic, or other blockchain analytics providers. The screening should evaluate:

- Source wallet risk scoring: Is the sending wallet flagged for sanctions exposure, illicit activity, or elevated risk?

- Transaction monitoring: Does the transaction pattern match known typologies for money laundering, terrorist financing, or other financial crimes?

Travel Rule compliance

For qualifying transactions, ensure that the required originator and beneficiary information is collected and shared with the receiving PSP or VASP (Virtual Asset Service Provider). This can be accomplished through multiple methods. Building Travel Rule compliance into the transaction layer rather than being handled as a separate middleware step, however, can reduce latency and operational complexity.

Auto Freeze for flagged payments

When compliance screening flags an incoming transaction, the funds should be held in quarantine automatically until a compliance review is completed. This prevents flagged funds from being credited to a merchant account before the issue is resolved.

Policy Rules

Configure policy rules specific to inbound flows:

- Minimum and maximum transaction thresholds

- Permitted stablecoin types and blockchains

- Automatic approval for acceptable-risk transactions (clean source wallet, below threshold, recognized payer)

- Manual review queue for flagged or high-value transactions

The goal is to build a compliance posture for stablecoin pay-ins that matches or exceeds what you maintain for card and bank transfer acceptance. The same governance standards applied to a new payment rail.

Step 4: Post-Receipt Processing

Once an inbound payment is confirmed and compliance-cleared, the next question is: what happens to the funds? This is where operational efficiency and the closed-loop advantage of stablecoin infrastructure become most visible.

Sweep received stablecoins from merchant accounts to your central treasury

Configure automated sweep rules per-transaction, hourly, or daily, based on your volume and operational preferences. Because each sweep costs pennies in the form of network gas fees and not the wire transfer fees that force batching in traditional treasury, you can sweep as frequently as your business requires.

Convert to fiat if the merchant prefers

Use the same off-ramp infrastructure you established in Blueprint 1 to convert received stablecoins to fiat and pay out to the merchant’s bank account. This leverages your existing liquidity provider connections without additional integration required.

Offer merchants optionality

Not every merchant wants the same thing. Some will want to hold stablecoin balances. Others will want immediate fiat conversion. Others will want a split, i.e. a portion held in stablecoin with the remainder off-ramped to fiat. The infrastructure supports all three models, and merchant preference can be configured at the account level.

Net settlement: the closed-loop advantage

This is where the two-way stablecoin payment engine becomes most powerful. Stablecoins received as pay-ins can flow directly into merchant settlement (Use Case 2) without converting to fiat and back again. You’re netting inbound and outbound stablecoin flows, which reduces on/off-ramp fees and eliminates unnecessary conversion cycles. Capital stays onchain longer, moving directly from where it’s received to where it needs to go.

Step 5: Pay-In Reconciliation

Reconciliation is where stablecoin pay-ins deliver a structural advantage over traditional payment methods, and where underprepared providers discover the gap that blocks scale.

Every pay-in reconciled against the merchant ledger in real time. Blockchain settlement data is validated and normalized for your ERP systems. Finance teams no longer manually match onchain transactions to merchant records. The deterministic nature of blockchain confirmation means there’s no ambiguity about whether a payment was sent, received, or still in transit.

Merchant-level aggregate reporting. Real-time visibility into pay-in volume by merchant, by stablecoin type, by blockchain, and by geography. This is the reporting your product and commercial teams need to understand adoption patterns, and the data your finance team needs to close the books.

Complete audit trail. Every inbound transaction produces an immutable, onchain record: from receipt to compliance screening to sweep to conversion (if applicable) to final crediting. This simplifies compliance reporting, audit preparation, and dispute resolution.

Use Case 2: Instant Merchant Settlement with Stablecoins

What you’re solving

Merchants wait 2-4 business days to receive funds from processed transactions, and even longer on weekends and holidays. In today’s competitive environment, that delay is increasingly unacceptable. Merchants need their capital to keep working: buying inventory, paying suppliers, covering payroll. Every day of settlement delay is a day their capital is locked.

Cross-border merchant settlement compounds the problem. Disbursing to merchants in different jurisdictions requires correspondent banking, prefunded accounts, and FX conversion. Each adds cost, time, and reconciliation complexity.

The competitive pressure is real. When a PSP competitor offers T+0 settlement and you’re still running T+2 or T+3, the merchant’s decision calculus is straightforward. Instant settlement is a merchant acquisition and retention tool.

The stablecoin advantage

- Freed liquidity. Less capital locked in prefunded settlement accounts means more capital available for productive use, whether that’s generating yield (Blueprint 1), funding additional transaction volume, or supporting geographic expansion.

- T+0 disbursement, 24/7/365. Settle with merchants in real time, not in banking-hour windows, not on a next-day cycle, not after a weekend delay. When a PSP disburses funds to merchants after processing consumer transactions, stablecoin rails allow settlement of what merchants are owed faster and across any corridor. The benefit to the merchant is clear: faster access to capital, better cash flow, stronger retention.

- Payouts to stablecoin wallets — no bank accounts needed. Merchants can receive settlement directly to a stablecoin wallet. This eliminates the requirement for the merchant to have a bank account in the settlement currency’s jurisdiction, which is a significant barrier for cross-border merchants. Foreign businesses that want to settle in USD, for example, often face difficulties opening US bank accounts due to compliance requirements. Stablecoin settlement removes that friction entirely.

- Eliminate correspondent banking fees for cross-border settlement. When you’re settling with merchants across borders, you’re replacing the correspondent banking chain and its stacking fees with a direct onchain transfer that costs pennies.

A Step-by-Step Implementation Blueprint for Stablecoin Merchant Settlement

Step 6: Extend Your Treasury Infrastructure for Merchant Settlement

You already have your vault architecture set up from the first blueprint: Corporate Treasury Optimization. Extending it for merchant settlement is a configuration exercise, not a new build.

Account Hierarchy

Create settlement-specific accounts within your existing hierarchy:

This mirrors the structure you’ve already built for treasury management, with an additional layer for merchant-specific settlement flows.

Account Structure

Choose your account structure based on your operational and regulatory requirements:

- Omnibus: Simpler operations. Funds are pooled, and an internal ledger tracks each merchant’s balance. Works well for high-volume PSPs with strong internal reconciliation systems.

- Segregated: Each merchant’s settlement funds are held in a separate account. Easier reconciliation, cleaner audit trail, and preferred for regulated environments where clear separation of merchant funds is required.

Configure policy rules for settlement flows

Approval thresholds, velocity limits, permitted asset types, and authorized signers. This is the same governance framework you established in Blueprint 1, extended to cover outbound merchant settlement. These rules should be enforced automatically on every settlement transaction via a policy engine.

Step 7: Build the Merchant Settlement Flow

This is where the merchant experience changes. Instead of waiting days for settlement, merchants receive funds in minutes or on whatever schedule you choose to offer.

Merchant Addresses

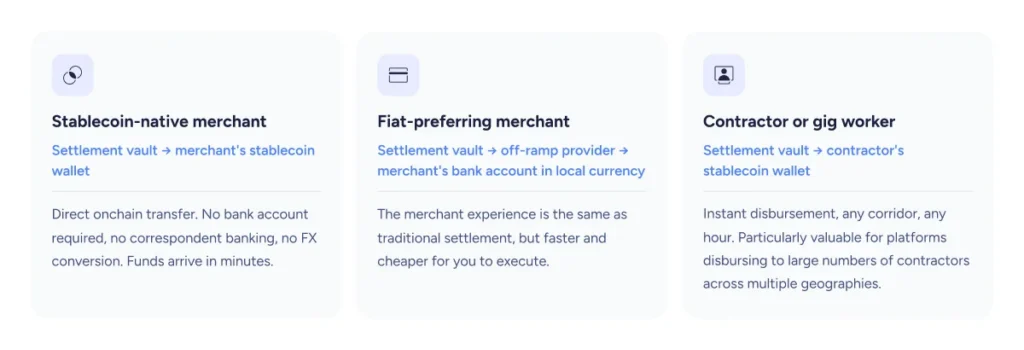

Whitelist merchant wallet addresses for merchants who want to receive stablecoin directly. For merchants who prefer fiat, configure off-ramp routes that convert stablecoin to local currency and pay out to the merchant’s bank account. Many PSPs will offer both options, letting the merchant choose their preferred settlement method.

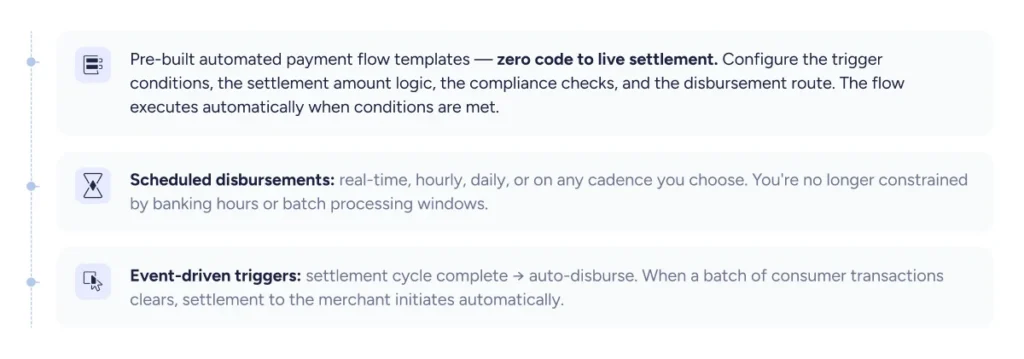

Settlement Triggers

Build settlement triggers using automation:

Compliance checks, liquidity routing, and reconciliation are embedded in every flow rather than bolted on as separate steps.

Settlement Vaults, Paths, and Notifications

Create transfers from your settlement vault to merchant wallets or to a connected account for off-ramp. The flexibility here is important: you can pay out from your own vault account, or directly from a connected account with a liquidity provider.

Example merchant settlement paths:

Configure webhook notifications so your internal systems receive real-time confirmation when each merchant settlement is complete. Merchants can see settlement status in their dashboard in real time.

Step 8: Configure Merchant Settlement Compliance

Outbound settlement compliance follows the same principles as inbound pay-in compliance, but applied in the other direction.

Transaction screening on every outbound settlement

AML, sanctions, and Travel Rule compliance are built into every transaction. This is a critical architectural distinction. When compliance is embedded at the transaction layer, it executes automatically and consistently. When it’s bolted on as middleware, it introduces latency, creates operational gaps, and becomes the first thing that breaks at scale.

Auto Freeze for flagged transactions

When compliance screening flags an outbound settlement, the disbursement is held automatically until review is complete. The merchant is notified, the compliance team is alerted, and the funds remain in the settlement vault until the issue is resolved.

Policy enforcement before execution

Enforce every compliance rule before any settlement transaction executes. This means approval thresholds, velocity limits, permitted asset types, and authorization requirements are checked programmatically.

Travel Rule compliance

Originator and beneficiary information is collected and shared automatically between VASPs as part of the settlement flow.

Step 9: Merchant Settlement Reconciliation

Reconciliation is where the operational advantage of stablecoin settlement becomes most tangible for your finance and operations teams.

Every merchant settlement can be reconciled in real time

MT94x and BAI2 reconciliation reports generated automatically, integrated into your ERP, and audit-ready from the moment the settlement is confirmed. This is enterprise-grade reconciliation in the formats your finance team already works with.

Deterministic onchain confirmations

Replace the uncertainty of traditional settlement reconciliation. With correspondent banking, you’re matching records across multiple institutions with different systems, different timing, and different data formats. With onchain settlement, there’s a single source of truth: the transaction was confirmed on the blockchain at a specific time, for a specific amount, to a specific address. No ambiguity. No pending states. No “it’s still processing.”

Real-time visibility into all settlement activity

Which merchants have been settled, which are pending, which are flagged — all visible in real time, not assembled from batch reports at the end of the day.

Merchant-level reporting

Balance, transaction history, settlement status, and settlement speed metrics. This is the data your merchant success team needs to demonstrate the value of stablecoin settlement, and the data your finance team needs to close the books.

Immutable audit trail

Every settlement produces an onchain record that can’t be altered or disputed. This simplifies audit preparation, regulatory reporting, and any settlement disputes with merchants.

What You’ve Built

By following the steps in this blueprint, you’ve built a two-way stablecoin payment engine for your PSP.

Money Flows

Money flows in through stablecoin pay-ins at approximately 0.5% acceptance cost versus 2-3% for card processing, with zero chargeback risk, T+0 confirmation, and geographic expansion that’s driven by software integration rather than acquiring bank relationships.

Money flows out through instant merchant settlement with T+0 disbursement 24/7/365, to stablecoin wallets or fiat bank accounts, in any corridor, without correspondent banking fees or banking-hour constraints.

Corporate Treasury

You already setup your treasury to be optimized, yield-generating and automated.

All three layers share the same wallet infrastructure, the same policy engine, the same compliance stack, and the same reconciliation layer. There’s no separate platform for pay-ins versus settlement versus treasury. The architecture is unified, which means every improvement to compliance, every new liquidity provider connection, and every automation rule benefits all three flows simultaneously.

The closed-loop advantage is the compounding effect: stablecoins received as pay-ins flow directly into merchant settlement without unnecessary fiat conversion cycles. Capital stays onchain, moves faster, and costs less to operate.

Once you’ve built pay-ins and merchant settlement, the next phase extends to embedded wallets, giving merchants their own stablecoin accounts inside your platform so they can receive, hold, earn yield, and transact natively without leaving your ecosystem. That’s the next blueprint in this series, and it builds entirely on the infrastructure you’ve deployed here.

Summary: Requirements for Stablecoin Pay-In and Settlement Operations

Implementing stablecoin pay-ins and merchant settlement requires the same institutional-grade infrastructure you deployed for treasury operations, extended to handle inbound and outbound payment flows at scale.

Launch speed that matches competitive urgency. The PSPs deploying stablecoin settlement today are doing it in weeks, not quarters. Pre-built payment flow templates, APIs in multiple languages, and a developer sandbox for testing mean your engineering team focuses on merchant experience and product differentiation rather than blockchain nodes and cryptographic key management.

Wallets that scale with your business. Payment companies process millions of transactions at all volumes. The infrastructure must handle high throughput, unexpected volume peaks, and any wallet configuration your business requires.

Reconciliation and reporting that finance teams trust. This is the gap that surfaces three months post-launch if you don’t solve it from day one. Manual reconciliation, audit-unfriendly blockchain data, and disconnected reporting are the silent blockers of scale. MT94x and BAI2 reconciliation reports, real-time ERP integration, and audit-ready reporting in the enterprise-grade formats your finance team already works with are non-negotiable for production operations.

Compliance embedded at the transaction layer. Both inbound pay-ins and outbound merchant settlement require compliance screening on every transaction, including AML, sanctions, and wallet verification. This must be built into the transaction flow, not applied as separate middleware. The compliance posture for stablecoin payment flows should match or exceed what you maintain for card and bank transfer operations.

Neutral infrastructure that doesn’t compete with your business. This matters more than it might seem at first glance. If your stablecoin infrastructure provider also operates an exchange, a consumer wallet, or a merchant checkout product, they’re competing with your merchants, and potentially with you.

A complete platform, not a point solution. Pay-ins and merchant settlement are two use cases on a longer roadmap. Embedded wallets, corporate treasury automation, cross-border payouts, and new financial products are all ahead. You need a platform that scales across use cases, geographies, and asset types without replatforming. Start with pay-ins and settlement. Expand from there. One platform, one integration, multi-year roadmap.

Fireblocks is world class on the security front. As our throughput scales, our diversity of payment types scale, and the complexity of what we do scales. It’s been game changing to be able to manage that in Fireblocks.

Ben O’Neill

Head of Payment Operations, Bridge

Who’s Already Moving

See how PSPs are deploying stablecoin pay-ins and merchant settlement today:

Checkout.com is actively deploying stablecoin merchant settlement and is referenced as a competitive benchmark in sales conversations across the PSP market. Their move signals to the broader market that stablecoin settlement is becoming standard infrastructure for tier-one PSPs.

Bridge cut bulk settlement from 12+ hours to under 90 minutes and processes millions of transactions in high-volume bursts on Fireblocks. What began as basic onchain custody evolved into full payment processing, token issuance, and automation. This demonstrates how a single infrastructure platform scales from one use case to a comprehensive payment engine.

Bloxcross uses Fireblocks as a unified platform to accept pay-ins, convert to stablecoins, and connect with liquidity providers for merchant settlement. They expanded their client base to over 2,000 merchants within a year of going live, delivering real-time cross-border settlement.

Triple-A, a licensed payments institution across the US, Europe, and Singapore, enables over 20,000 businesses to accept both fiat and digital currency payments on Fireblocks. Their scalable API integration and automated gas management reduced operational overhead while expanding merchant coverage.

By following the steps in this blueprint, you’ve built the two core payment flows for a stablecoin-enabled PSP on the treasury foundation you already deployed. The next phase extends this to user accounts via embedded wallets, where merchants get their own stablecoin accounts inside your platform. This unlocks new revenue streams, deeper merchant relationships, and a competitive moat that goes beyond settlement speed.