Introduction: Beyond the Transaction

Using stablecoins for treasury optimization transformed your internal operations with faster settlement and improved capital efficiency. With that foundation in place, your business has the know-how to extend that same stablecoin infrastructure directly to end consumers to unlock new revenue streams and competitive differentiation.

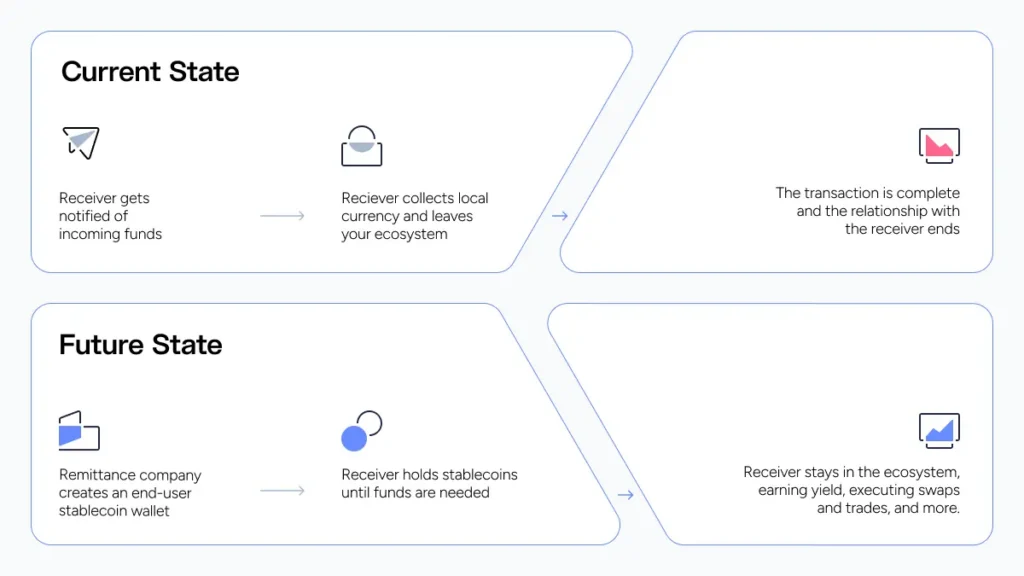

The current model doesn’t capture both sides of a transaction: when a customer sends money, you facilitate the transfer, the individual receiver cashes out immediately, and the relationship ends. You only capture one transaction fee.

Stablecoin payment accounts (ie, wallets) create an entirely new model. Give receivers a place to hold stablecoin balances, and you transform from a transaction facilitator to a financial services platform simply by integrating embedded wallets without the complexity. They can store value, earn yield, make payments, and access financial services all within your ecosystem, creating a new business model with ongoing customer relationships and multiple revenue streams.

This blueprint provides a practical implementation guide for receiver wallet expansion.

Use Case: Receiver Wallet Creation

Current state:

The receiver gets a notification, picks up the cash, and leaves your ecosystem once the transaction is complete.

The opportunity:

Not all receivers need funds immediately. Many receive regular remittances for things like monthly support, education funding, or other types of recurring payments. They convert to cash not because they need it all today, but because they have no better option.

When remittance companies are leveraging stablecoins for a cross-border transaction, that transaction doesn’t need to “stop” at the stablecoin. Instead, remittance companies can hold the funds within the digital ecosystem. By doing so, they unlock a suite of financial tools for receivers that solve for more than just immediate liquidity, including:

- Store balances in stablecoins: In high-inflation markets, USD stablecoins preserve purchasing power, act as a hedge against inflation, and provide access to USD that may not otherwise be available. A receiver in Turkey or Argentina has clear incentive to hold USD-denominated balances without requiring a US bank account.

- Earn yield while waiting: Stablecoin balances generate returns through integrated yield products. A receiver holding $500 earning 4% APY generates $20 annually, which is meaningful money in many remittance markets.

- Execute swaps and trades: Convert between stablecoins, swap into other digital assets, adjust positions based on currency movements. Your wallet becomes an active financial management tool.

- Convert on their own terms: Need 200 pesos for groceries? Convert just that amount. Keep the rest in USD for next week. This flexibility has real economic value.

- Access financial services: Bill pay, P2P transfers, savings products, merchant payments, and lending all become possible with wallet infrastructure.

The Embedded Wallets Advantage

Before we dive into how to implement receiver wallets, let’s explain what all this means and how various wallet types differ. The main difference between custodial and non-custodial (embedded) wallets is who controls the private keys.

Custodial Wallets

Custodial wallets are controlled by a third party that manages the private keys on your receiver’s behalf. Managing the funds of all users globally creates regulatory and licensing complexity.

Alternatively, if a user is receiving funds in an external wallet such as MetaMask or Phantom to manage their own funds, they need to have a deep understanding of blockchain and crypto, manage seed phrases, and be able to navigate complex UX. This creates massive friction and a steep adoption curve for most receivers.

Embedded Wallets

Embedded wallets, or non-custodial wallets, eliminate this entirely. They are built directly into the remittance company’s specific application, where receivers retain control of their private keys and funds, and don’t have to bring an external wallet or manage seed phrases. The remittance company is not responsible for custodying funds or needing to be deeply familiar with blockchain transaction interactions. Users can onboard and sign in with just an email or social media account.

A seamless UX means receivers see familiar payment account experiences such as balances, transaction history, and simple send/receive without knowing about blockchain infrastructure underneath. In addition, transaction sponsorship (i.e. when a designated account covers the gas fee) further lowers the barrier to entry and reduces user complexity, making it seamless for users that don’t need to hold native tokens or be familiar with the underlying blockchain technology in order to interact.

This reduces the remittance provider’s operational and regulatory burden associated with custodying customer assets, while enabling you to offer revenue-generating products based on those assets. When receivers hold stablecoin payment accounts via embedded wallets, you can layer on spend capabilities (cards), save capabilities (yield products), and trade capabilities (swaps)—all out-of-the-box with the right infrastructure provider.

A Step-By-Step Operational Blueprint

Step 1: Deploy Receiver Wallet Infrastructure

Leverage embedded wallet technology:

Integrate embedded wallet infrastructure that puts users in control of their assets, while you control the customer experience and branding. Deployment can be as simple as installing a widget that’s embedded directly into your website or app.

For institutional-grade security and sub-second signing, leverage TSS-MPC technology and hardware isolation with multiple authentication factors, behavioral analytics, and velocity limits.

Design account creation flows for your customer:

Remittance receivers onboard to your app with a simple, familiar account experience that you control, with their embedded wallet created invisibly behind the scenes. The process for setting up a wallet is as easy as the process of setting up an account within your app today. Users can register instantaneously with their email or phone, basic identity information, and a verification code. No seed phrases or blockchain knowledge required, abstracting away complexity. The main difference is that the embedded wallet layers on entirely new hold and spend capabilities that weren’t previously available.

Enable receiver settlement: Configure systems to send stablecoins directly to embedded wallets you’ve created on the receivers’ behalf. Instead of cash pickup notifications, settle funds instantly and directly into the wallet balance 24/7, with a complete audit trail.

Ensure compliance requirements: All wallet operations carry necessary AML/KYC checks, sanctions screening, and transaction monitoring integrated into wallet onboarding. It’s crucial to implement robust transaction monitoring and enhanced due diligence.

Connect external accounts: Enable receivers to link their embedded wallet to their favorite exchange, financial application, or another external wallet, allowing receivers to add funds beyond incoming remittances.

Step 2: Offer Storage and Yield Capabilities

Enable receivers to hold USD stablecoin balances:

Enable receivers to hold USD stablecoin balances in their wallets instead of forcing immediate conversion to local currency. When remittances arrive, funds automatically settle into the receiver’s stablecoin account where they can be stored and used for saving, sending and earning capabilities. This shifts control from your operational schedule to the receiver’s actual cash needs.

Integrate staking and yield products:

Allow receivers to generate yield on the stablecoins in their wallets. Connect to yield-generating products including staking, treasury products, DeFi savings in one click. Customer sees: “Earn 4% APY on your USD balance.”

Self-service conversion:

Receivers convert on their terms. Partial conversions, scheduled conversions, or on-demand as needed. This means the receiver can optimize for currency fluctuations or protect against inflation as much as possible.

Liquidity Management:

It’s important to maintain relationships with multiple liquidity providers, from exchanges to OTC desks. A multi-provider strategy ensures your stablecoin payments are geographically and asset inclusive, cost-efficient, and technically resilient. By diversifying, you can access the best exchange rates and local currency corridors globally while eliminating the risk of a single point of failure.

Step 3: Customer Protection

Building trust requires a comprehensive customer protection framework.

Wallet terms of service must clearly explain product risks, fee structures, rights and responsibilities, and dispute resolution processes in plain language customers actually understand. To further demonstrate commitment to customer safety and increase confidence in your platform, the app should also implement transaction policies (e.g. whitelist safe, reputable tokens) and protection from malicious smart contracts as means of mitigating operational failures, security incidents, or service disruptions.

All fees should be disclosed transparently before customers commit to transactions, with no hidden charges or surprise costs that erode trust and create support burden. Implement fast dispute resolution processes that allow customers to quickly report unauthorized activity or resolve issues, as responsive treatment generates satisfaction and reduces regulatory scrutiny.

Finally, robust data privacy frameworks compliant with GDPR, CCPA, and local privacy regulations are non-negotiable. Customer financial data requires the highest level of protection, and transparency about data usage with customer control over their information builds the foundation of long-term trust.

Revenue Model Transformation

Customer Lifetime Value Expansion

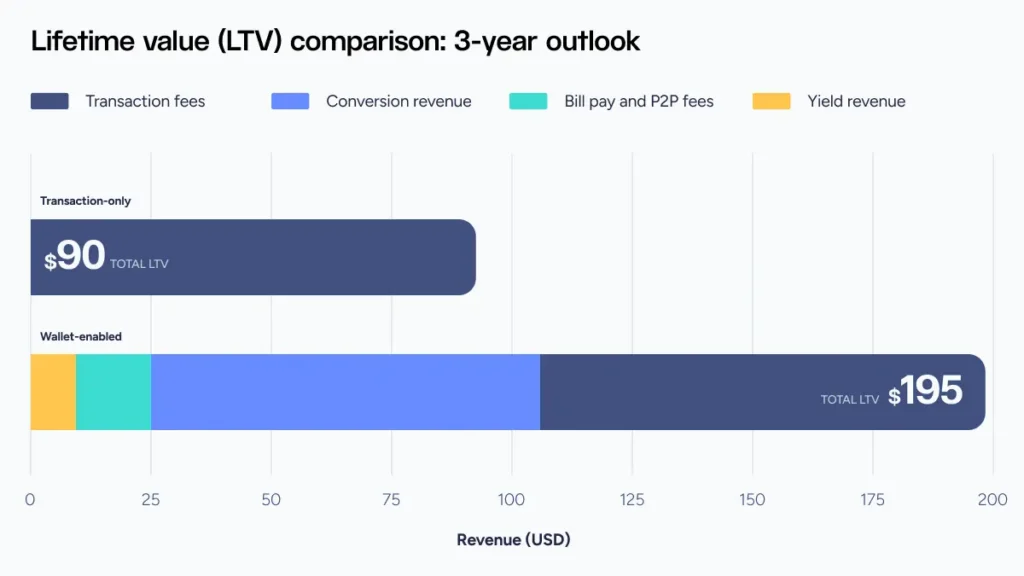

Transaction-only model: $75-110 in lifetime transaction fees over 3 years (assuming 36 monthly remittance transactions at $2-3 average margin per transactions).

Wallet-enabled model (same customer over 3 years):

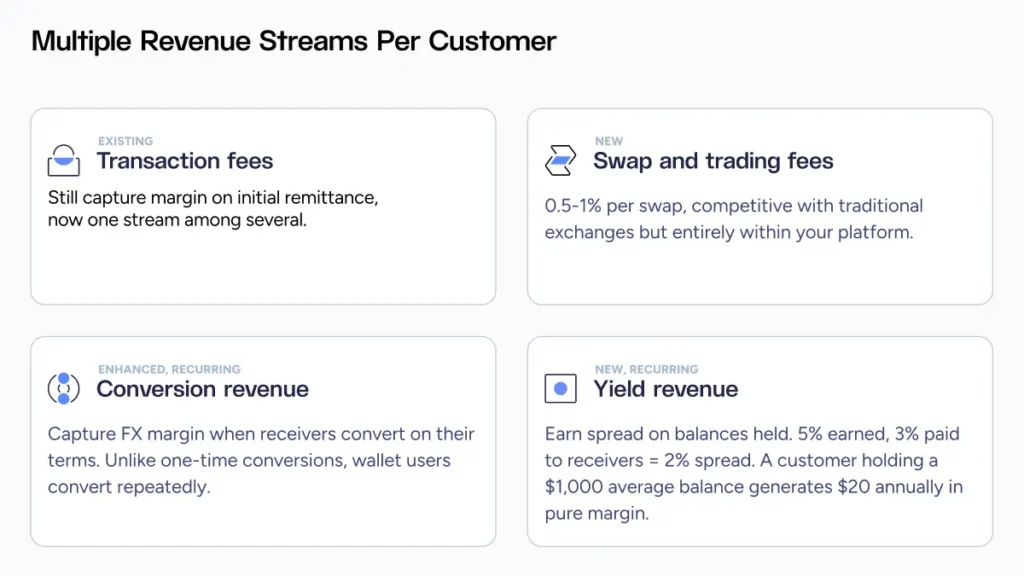

- $90 transaction fees – same 36 monthly remittances at $2.50 average margin

- $9 storage revenue – average $150 balance maintained over 36 months, earning 2% yield spread (5% earned on stablecoin treasury, 3% paid to receiver) = $3/year x 3 years

- $81 conversion revenue – 90 partial conversions over 3 years (averaging 2.5 conversions per month as receiver gradually pulls funds) at $100 average conversion amount with 3% FX margin = $3 per conversion x 27 conversions (the other 9 conversions covered by the $300 monthly inflow)

- $15 bill pay and P2P fees – 40 bill payments over 3 years at $0.25 average fee ($10 total) + 10 P2P transfers at $0.50 average fee ($5 total)

Total: $195—approximately 2X the transaction-only model.

Wallet users have high switching costs. Moving to a competitor means new accounts, transferring balances, updating configurations, disrupting patterns. Retention rates exceed transaction-only customers, even based on these modest estimates.

Competitive Advantages

Receiver wallets create differentiation that transcends price competition. While competitors can match your transaction fees, they can’t instantly replicate an ecosystem with cards, bill pay, P2P transfers, and financial services. The more products receivers use, the higher the switching cost.

This ecosystem approach transforms customer economics dramatically:

- Wallet customers generate 10x the lifetime value of transaction-only customers, fundamentally changing acquisition economics.

- Your existing remittance flow becomes the distribution channel for wallet adoption, allowing you to leverage existing CAC to build a higher-value business rather than paying incremental acquisition costs.

- Network effects compound these advantages; P2P transfer capability means every new wallet user makes the platform more valuable for existing users, while merchant acceptance creates a two-sided network that’s increasingly difficult for competitors to match.

The data advantage further widens the gap: understanding receiver behavior, spending patterns, and financial needs provides competitive intelligence that informs product optimization and strategic decisions competitors simply don’t have access to.

Finally, the compliance infrastructure, multi-market licensing, and operational excellence required to run wallets at scale create meaningful regulatory moats—new entrants face years of development and significant investment to replicate these capabilities.

By layering on spend capabilities and enabling swaps and trading, this gives remittance companies the opportunity to access the following capabilities:

Attach cards to wallets: Integrate with card issuance partners for physical or virtual debit cards linked to stablecoin balance. Wallet transforms from storage to active spending tool.

Seamless conversion at point of sale: Card automatically converts required stablecoins to local currency at transaction moment. The receiver experiences a normal debit card anywhere that Visa is accepted. The merchant receives normal local currency, while stablecoin infrastructure remains invisible.

Cross-border spending: Cards work internationally without traditional foreign transaction fees. Lower FX spreads than traditional banking cards create value for receivers while generating conversion revenue.

Spending controls: Enable receivers to set limits, transaction categories, geographic restrictions. Gives control while reducing fraud risk.

Built-in Cross-Chain Swaps: Allow swaps between stablecoins or exchange for other digital assets. Present in familiar terms: “Exchange USD Digital Cash for EUR Digital Cash.”

Simple interface: Show real-time rates, fees, final amount. Make the process as simple as a traditional money transfer, but instant and with better rates.

Position adjustment: Receivers can swap stablecoins into other tokens or even tokenized financial assets such as stocks, as a way to truly construct a diversified onchain portfolio rather than simply holding different receipts of USD.

Summary: Requirements for Receiver Wallets

Wallets are the new application layer. Implementing receiver wallet operations requires institutional-grade infrastructure that meets the security, compliance, and operational requirements while maintaining seamless user experience for mass-market customers.

- Embedded Wallet Infrastructure: Deploy non-custodial embedded wallets that put users in control of their assets while you control the customer experience and branding. Deploy an infrastructure that handles MPC-based key management and institutional-grade security invisibly, enabling you to offer revenue-generating products (storage, yield, cards, swaps) without the operational and regulatory burden of custodying customer assets.

- Seamless Onboarding and User Experience: Wallet creation must happen invisibly during user registration, ideally under two minutes with email or phone, basic identity information, and verification code. Mobile-first design optimized for lower-end devices common in remittance markets ensures accessibility.

- Integrated Compliance Framework: Compliance should be embedded directly into wallet operations from day one. KYC/AML workflows integrated into onboarding, transaction monitoring for enhanced due diligence, sanctions screening on all operations. Integrations with Notabene, Elliptic, and Chainalysis enable Travel Rule compliance for cross-border stablecoin transfers, wallet verification, and AML/KYT checks. Built-in fraud detection capabilities including velocity limits, behavioral baselines, device fingerprinting, and network analysis for money laundering patterns address the higher risk profile of wallet operations versus traditional remittance.

- Liquidity and On/Off-Ramp Connectivity: Enable receivers to connect external bank accounts or payment methods through the Fireblocks Network for Payments. A single, pre-configured ecosystem integration point provides access to multiple vetted partners across the entire wallet value chain (liquidity providers, on/off-ramps, card issuers, yield protocols, compliance solutions, payment networks) and across geographies, dramatically accelerating deployment and reducing technical maintenance. New markets, products, or partnerships can be activated in days rather than months, and mass payout capabilities allow you to settle stablecoins directly into receiver embedded wallets instantly, 24/7, with complete audit trails.

- Yield and Staking Integration: Connect receivers to yield-generating products through staking and DeFi ecosystem integrations. Support for secure native staking, treasury products, and audited DeFi protocols enables tiered yield structures (instant access at 2% APY, locked terms at 4-5%) without requiring you to build direct protocol integrations. A provider like Fireblocks handles the smart contract interactions while you control the customer-facing product experience and capture yield spreads.

- Swap and Trading Capabilities: Enable in-wallet exchanges between stablecoins or other digital assets through liquidity aggregation and trading infrastructure. Simple interfaces show real-time rates, fees, and final amounts while sophisticated receivers can hold balances across multiple stablecoins or adjust positions. This transforms wallets into personal treasury management platforms without requiring you to build exchange functionality from scratch.

- Operational Simplicity at Scale: As wallet operations grow from pilot markets to global deployment, you need infrastructure that scales without architectural changes. The same security model, policy engine, and operational workflows that manage pilot programs should work identically at production scale. Real-time balance tracking, comprehensive transaction history, and API access integrate with existing accounting and ERP systems. Because all stablecoin transactions are recorded onchain, reconciliation becomes significantly simpler than traditional financial systems.

- Customer Protection Framework: Robust data privacy frameworks compliant with GDPR, CCPA, and local regulations are built into the infrastructure layer. Support for customer protection insurance, reserve funds, transparent fee disclosure, and fast dispute resolution processes. Multi-layered security architecture with hardware isolation, behavioral analytics, and proactive threat detection protects customer funds while maintaining seamless user experience.

By following the steps laid out in parts one and two of our remittances blueprint, you’ve now transformed treasury operations with stablecoins, and unlocked new customer-facing innovation by enabling receiver wallets. Next we’ll focus on extending stablecoin benefits to offer new financial services including bill pay, P2P transfers, lending and credit, and more.

Request a demo to discuss your stablecoin strategy with our payments experts today.