At HederaCon and Consensus in Miami this May, every conversation I had with banks circled back to the same problem: the blockchain strategy discussion has evolved into a future proof infrastructure decision that is still unresolved at most institutions.

That’s not the conversation banks were having two or three years ago. Back then, the internal debate centered on ROI, use case validation, and whether digital assets were worth the organizational attention. It’s the classic “can we make money off of crypto trading?”

What I’m hearing now is different: US banks have moved past the commitment question and into technology strategy. What do we need to build? In what sequence? How do we connect it to the systems and processes we already run? We are seeing blockchain, along with AI, forcing banks to reevaluate their traditional businesses to recalibrate against the competitive surge from neobanks and fintechs.

The Financial Grid, our 2026 flagship survey of 600+ C-suite and senior decision-makers at financial institutions and corporates globally, documents how far that shift has gone across the industry. The Financial Grid USA is the regional cut of that research, mapping what it looks like specifically for American banks: where they are building, what is blocking them, and why the infrastructure decisions they make in 2026 will determine how fast they can scale.

The central finding: US institutions have chosen their entry point, and the constraints are no longer external.

The US Entry Point Is Already Decided

While many large regional and global banks have multiple business lines and revenue streams, deposits and payments sit at the core of every bank. No other region is building toward institutional-scale stablecoin issuance at this speed or this ambition. 68% plan to issue their own stablecoins in a live environment in 2026, against 36% in Europe and 11% in APAC. 79% plan to deploy stablecoins issued by other regulated institutions alongside their own.

The use cases that follow from that decision are equally specific. 99% of US institutions rate 24/7 settlement as a high or core strategic priority. 90% rate internal settlement using tokenized deposits at the same level. This is a market that has decided what it is building and is now working out how to build it.

The questions we get from banks have moved on from the use cases for digital assets. They are about custody architecture and whether core systems can be connected to wallet infrastructure without a multi-year rebuild. Infrastructure sequencing questions. That is the conversation that has replaced the ROI debate.

The Mindshare Shift: From Business Case to Technology Strategy

The data makes the internal shift visible. Security functions are now leading digital asset initiatives at 30% of US financial institutions. Risk and compliance at 22%. Fewer than 2% of either function report no engagement at all.

The functions that spent years as the primary brake on digital asset programs are now among the most active participants in the build. And the most convinced: 99% of US institutions expect the regulatory direction to be favorable.

GENIUS introduced a national regulatory floor for stablecoin issuers. CLARITY is expected to complete the federal market structure framework. The institutions that were waiting for regulatory clarity are now building to known specifications. When security and compliance are reading incoming frameworks as build specifications rather than reasons to wait, the internal dynamic at a bank changes fundamentally.

This is what the mindshare shift actually looks like from inside the institution. The blocker has shifted from focus on the business case and the regulatory environment to the technology strategy: what to build, in what order, and whether the existing architecture can support it.

The Legacy Infrastructure Problem Is Real, and US Banks Know It

At my HederaCon panel on connective tissue and interoperability, I made an observation that got immediate recognition from the bankers in the room: if you talk to almost any bank, they will tell you their existing core infrastructure will not support a digital future. Plugging into wallets is difficult. Enabling real-time settlement on a batched database legacy architecture is harder still.

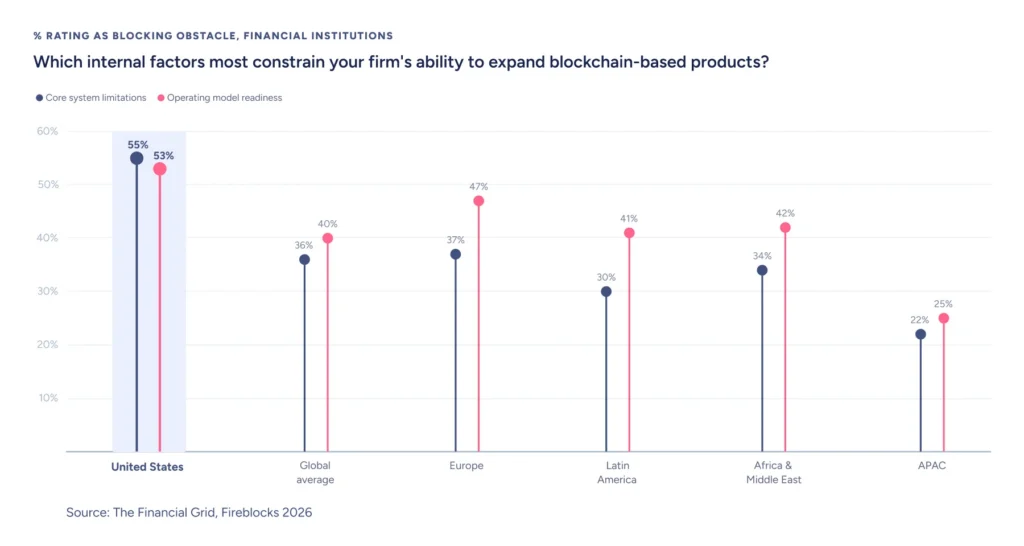

The Financial Grid USA puts numbers on that recognition. 55% of US institutions cite core system limitations as a blocking obstacle, the highest rate of any region globally. 53% cite operating model readiness as a blocking obstacle, against 40% globally.

And yet 86% have already committed or plan to commit budget in 2026, before CLARITY has passed. US institutions are absorbing the cost of foundational infrastructure work now, ahead of the final regulatory specification, because they understand what the sequencing requires. This is the work that doesn’t need CLARITY to begin: core systems, operating model, custody. That work is what positions an institution to move at speed when the full framework lands. The institutions resolving those constraints now will face a shorter path to production than those that wait.

What Provider Selection Reveals About the Build

The US data on infrastructure provider selection carries a finding that doesn’t appear anywhere else globally: the US is the only market where the ranking inverts. Globally, custody leads provider selection criteria at 61%. In the US, connectivity across blockchains, payment rails, and external providers leads at 66%. Custody is second at 60%. Integration with existing bank systems is third at 51%.

The inversion is not accidental. Operating on both sides of the stablecoin market simultaneously—issuing your own and deploying those of other regulated institutions—requires payment rail connectivity at a scale and scope that no other regional build currently demands. Across every factor on the list, 96-100% of US institutions rate each criterion as critical or important. US institutions are selecting for a provider that can deliver across the full stack, because the full stack is what the build actually requires.

The mindshare of US financial institutions has shifted. The technology strategy conversation is the one happening now, in every bank I talk to. The infrastructure decisions being made in 2026, on custody architecture, wallet governance, core system integration, and reporting, are the decisions that determine which digital asset businesses a bank can run, and whether it can run them at scale when the framework fully lands.

The institutions that get the sequencing right this year will have a shorter path to every digital asset use case that follows, whether it’s stablecoin issuance today or tokenized securities tomorrow.

Fireblocks works with 95+ banks building digital asset infrastructure. Read The Financial Grid USA report for the full regional data, and speak with our banking team about where your institution is in the build.