The global financial system runs on infrastructure that took decades to build, from payment rails and custody and settlement system, to trading infrastructure and regulatory and governance frameworks. Together, it forms a grid: the interconnected system through which value moves, settles, and is held across institutions, borders, and asset classes.

Banks, as well as their non-bank competitors, are now integrating a new layer into that grid: the capacity to move, hold, issue, and settle digital assets. The Financial Grid tells the story of where that build stands today, based on the 2026 Fireblocks survey of over 600 decision-makers at financial institutions and corporations.

Part 1 establishes that the investment decision in digital asset infrastructure has been made across the market. Part 2 maps where institutions are starting from: the use cases, asset types, and infrastructure choices already in motion. Part 3 defines what production-ready actually requires from banks. Download a pdf version of the report here.

Part 1: The Decision Has Been Made

The Digital Asset Infrastructure Build is Already Funded.

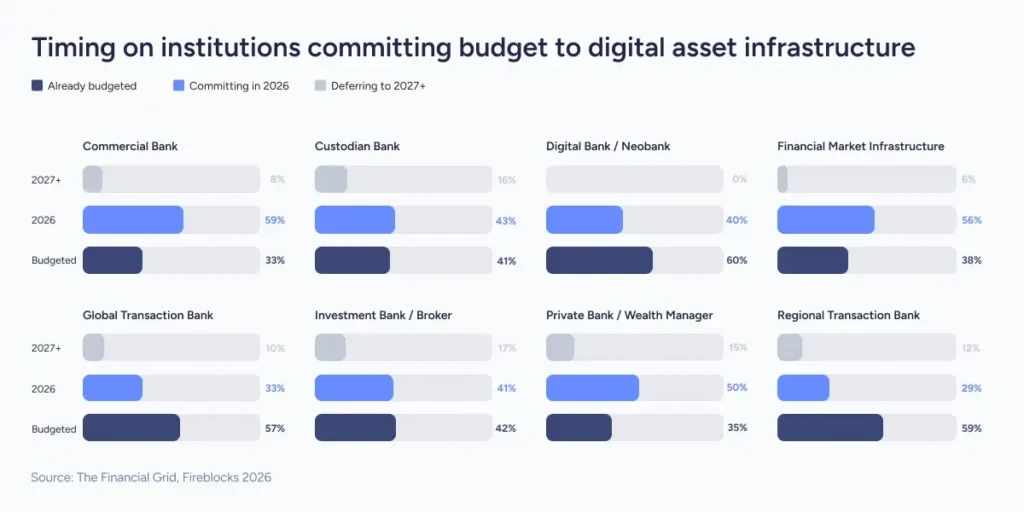

88% of financial institutions have committed or will commit budget to digital asset infrastructure in 2026. Only 11% are deferring to 2027, and virtually none beyond that.

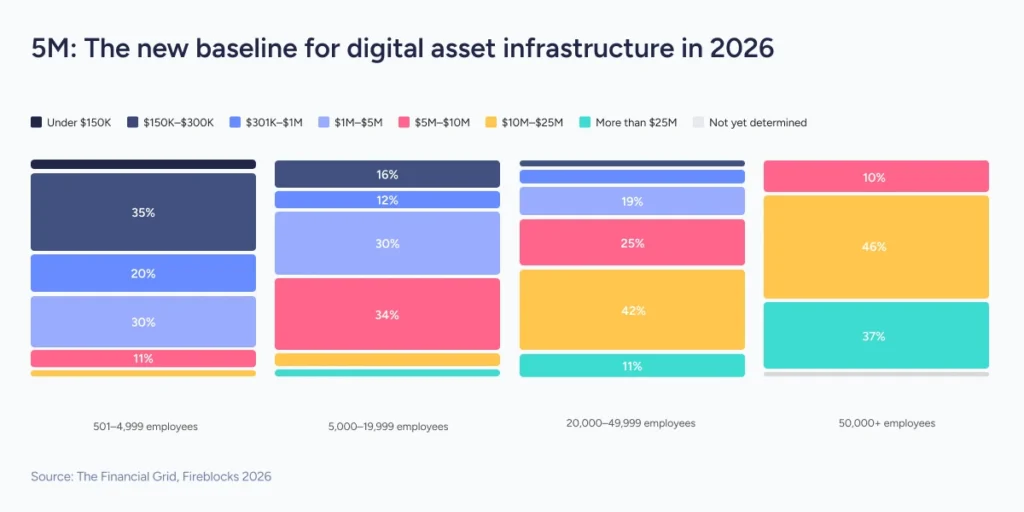

The scale of that commitment reflects production intent, not exploration. Among institutions that have sized their investment, 53% are spending $1 million or more. Within that group, 33% are spending between $5 million and $10 million, and 18% between $10 million and $25 million.

This is infrastructure spending at the scale that production decisions require. Even mid-sized institutions are committing at production scale: 72% of banks with 5,000–19,999 staff are spending $1 million or more. These are not pilot budgets.

Digital banks and neobanks lead on budget already committed at 60%, followed by regional transaction banks at 55% and global transaction banks at 57%. For digital banks, digital asset capability is core to the product.

The sectors deferring longest reflect a more complex infrastructure starting point, not a lower level of intent: investment banks at 17%, custodians at 16%, private banks and wealth managers at 15%.

Financial Infrastructure Transformation Outranks Every Other Driver.

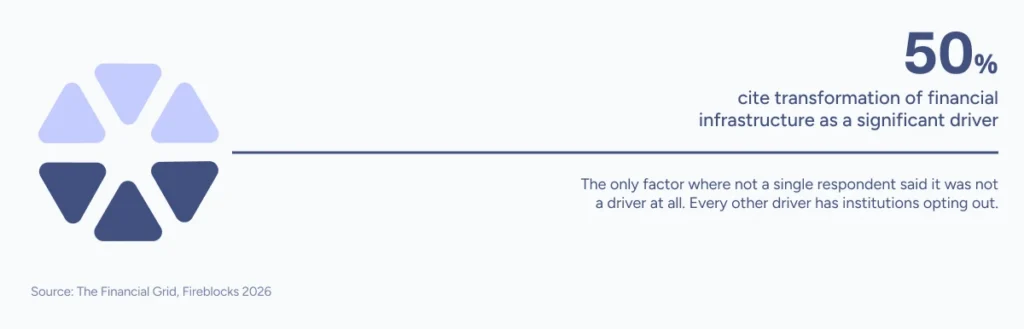

Banks are moving because the Financial Grid is being rewired beneath them. Financial infrastructure transformation is a significant driver of their digital asset strategy for 50% of respondents. It is the only driver where not a single respondent said it was not a factor at all.

Digital asset infrastructure has become the next layer of a build that began with core banking modernization, continued through internet banking, and is now extending to the onchain settlement and digital money capabilities that the next decade of financial services requires now.

The Sectors Moving Fastest Share One Thing: C-Suite Ownership.

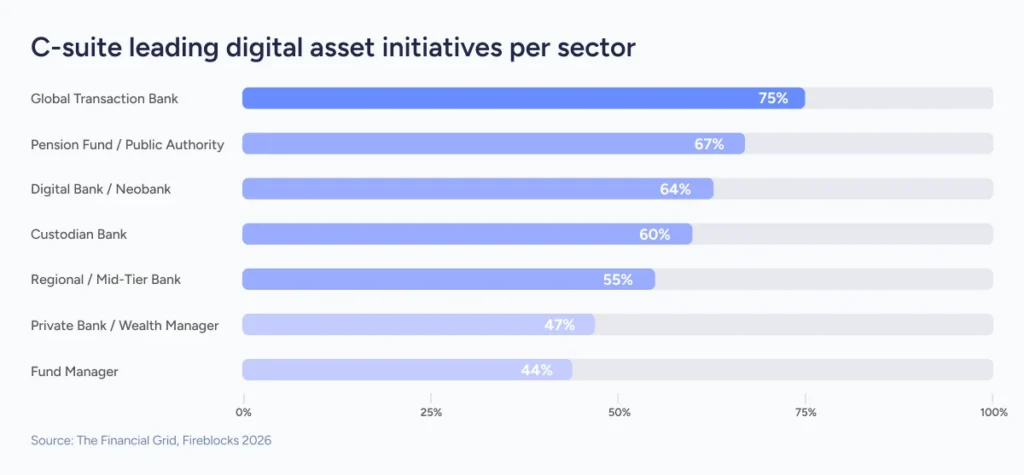

At 55% of financial institutions, C-suite executives are leading blockchain and digital asset initiatives directly. IT and architecture functions follow at 42% and Treasury at 35%.

C-suite ownership changes the pace of everything, from internal approvals and budget allocation to vendor selection. The institutions moving fastest on the infrastructure build are disproportionately the ones where that ownership sits at the top.

Infrastructure transformation at this scale is a board-level decision. And the C-suite is not just leading these programs. They are among the most convinced of their necessity.

The Existential Threat: It’s Not Other Banks.

43% of financial institutions identify non-bank competitive pressure as the critical driver of their digital asset investment. Only 24% say the same about pressure from other banks. The threat forcing the pace is not coming from peer institutions. It is coming from fintechs, payment providers, and digital asset platforms that are gaining market share with new offerings, and simultaneously represent the most demanding client segment that financial institutions serve.

By sector, digital banks and neobanks feel it most directly at 68%: they are building on the same infrastructure as the competitors they are racing against. Regional transaction banks follow at 50%, global transaction banks at 48%.

By institution size, mid-tier banks feel this most acutely: 48% rate non-bank pressure as critical, the highest of any size band. They are the most exposed, with pressure from both directions: agile fintechs attacking from below with lower-cost, faster-to-deploy digital asset products, and resource-rich Tier 1 banks from above with the capital to build proprietary infrastructure at scale. Mid-tier institutions are responding with urgency.

The Industry Is Building To Regulation, Not Waiting For It.

96% of financial institutions expect upcoming regulations to be favorable or very favorable for digital asset adoption in 2026. That near-unanimity marks a decisive shift. Regulation has moved from blocker to build specification.

MiCA in Europe, the GENIUS Act and OCC interpretive guidance in the United States, MAS and HKMA frameworks in APAC, VARA in the UAE exemplify the technical requirements that compliant digital asset infrastructure must meet.

In Fireblocks’ State of Stablecoins 2025, fewer than one in five firms cited regulation as a barrier, down from 80% two years prior. That shift has held. And accelerated. Banks that were waiting for regulatory clarity are now building to known specifications.

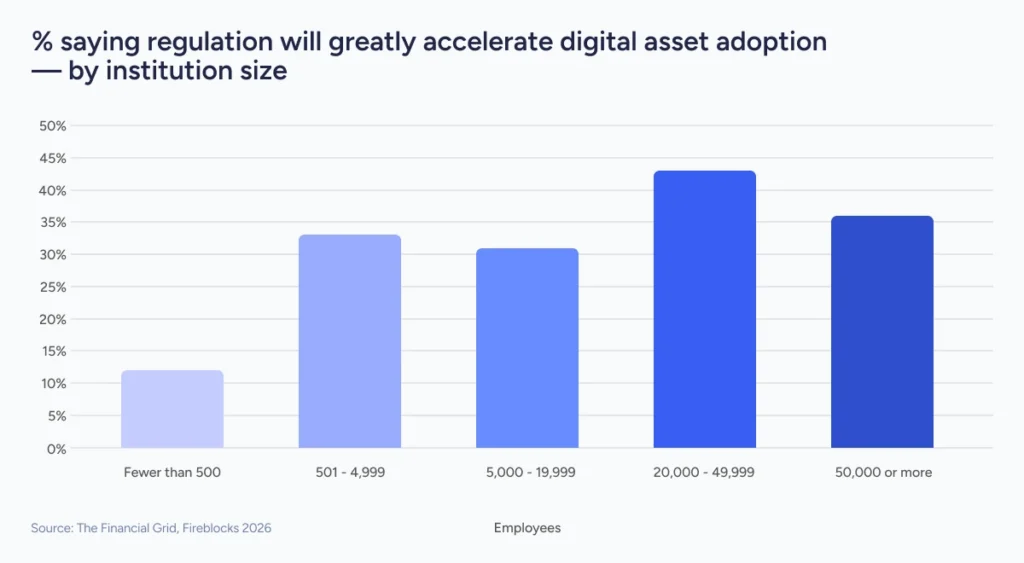

Regulatory clarity does not land the same way everywhere. Among the largest financial institutions, favorable regulation confirms a build already underway. Among the smallest, it remains a precondition: only 12% of institutions with fewer than 500 staff say regulation will greatly accelerate their adoption, compared to 43% among large D-SIBs and major regionals.

Part 2: Where Banks Are Starting Their Digital Asset Infrastructure Build

The commitment to build digital asset infrastructure is settled across the market. What is not settled is how far that build has progressed, what it is being built for, and where each institution is starting. This survey asked financial institutions not only what they are spending, but where they stand on the adoption curve and which use cases are driving their build priorities.

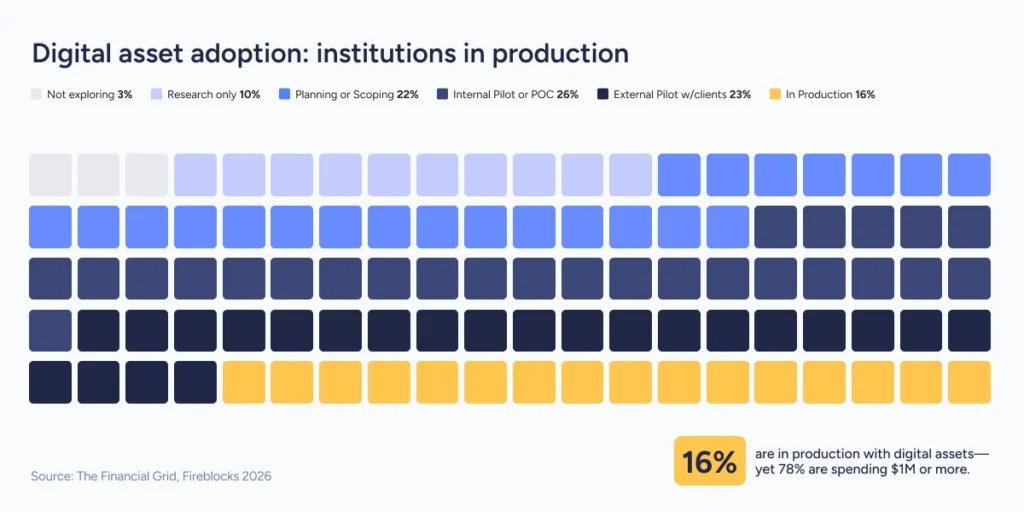

53% Are Spending At Production Scale. 16% Have Reached It.

The 2026 survey asked financial institutions to place themselves on the adoption curve, not in aggregate, but twice: once as an issuer of digital assets, and once as a user.

The distinction matters. An institution operating as a user is integrating digital asset capabilities into existing workflows. An institution operating as an issuer is building the infrastructure to originate, manage, and settle digital assets on its own balance sheet. They both need the infrastructure now.

As users, 19% of financial institutions are in production. As issuers, 14% are. The gap between those two figures reflects where most banks are in 2026: further along in consuming digital asset infrastructure than in originating it.

With both profiles taken together, more than half of financial institutions are still in pilot or planning. Only 16% have reached production.

The gap between investment and production is the defining characteristic of this market moment: 53% of financial institutions are spending $1 million or more on digital asset infrastructure this year. That is production-scale spending: vendor selection, architecture decisions, systems integration, staffing, and regulatory compliance work. That is not exploration spending. It is conversion spending, and it signals a market that is moving from commitment to build. But the build is not ready.

Getting there requires the right infrastructure decisions, the right architecture choices, and the right entry point.

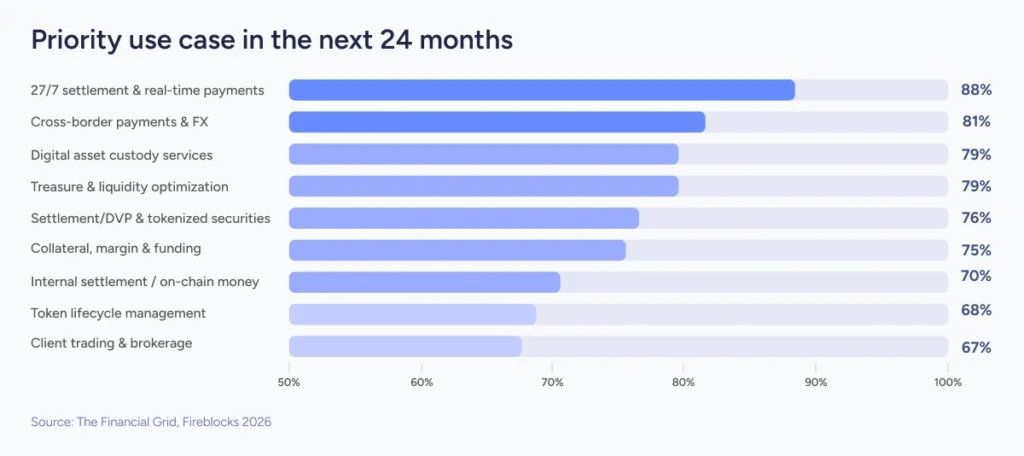

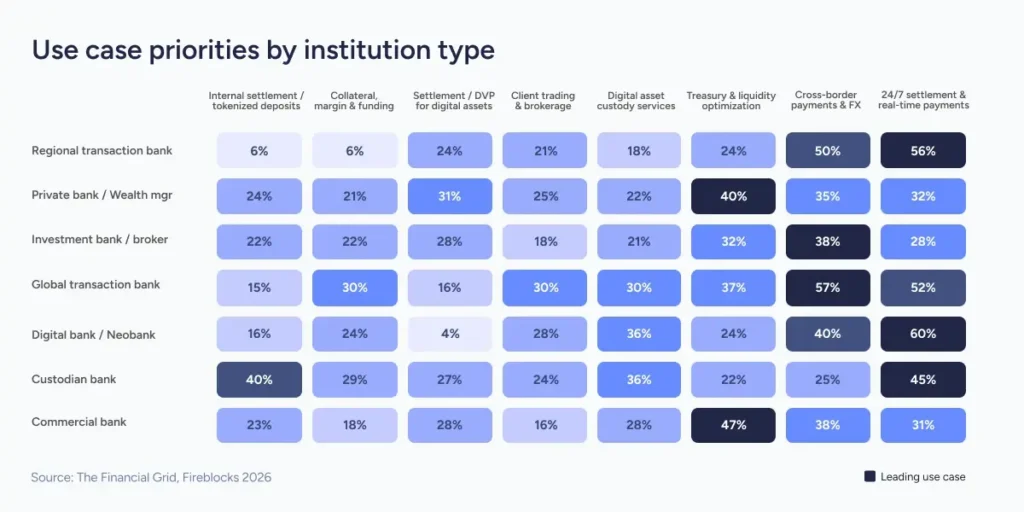

The Use Case A Bank Prioritizes First Is The One Its Business Can’t Afford To Lose.

Payments-related use cases lead the priority ranking, but only marginally. The more important signal is that institutions are not treating digital asset strategy as a single use case decision. They understand they will implement across multiple use cases, and their entry point reflects where their business is most immediately exposed. At the core strategic priority level, the differentiation by institution type shows intentionality.

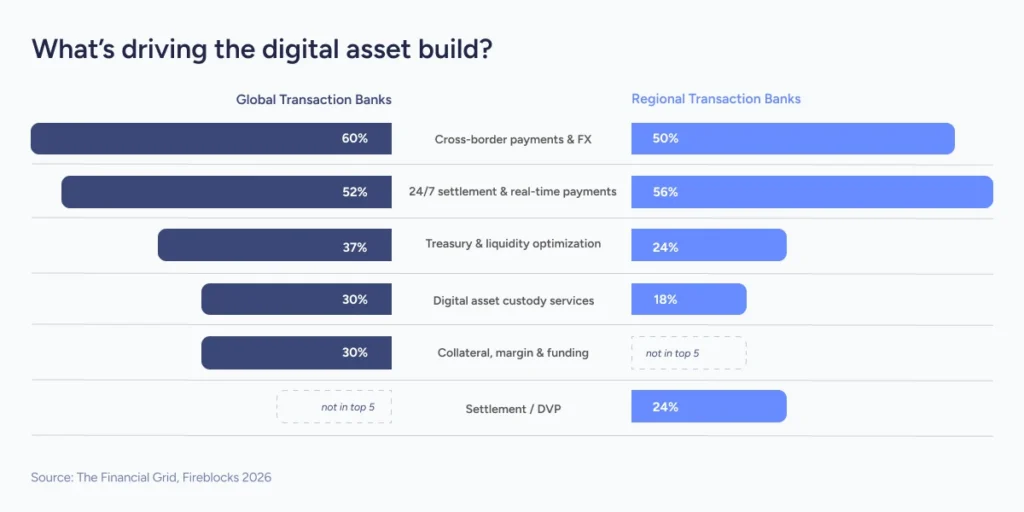

Global transaction banks (GTBs) and regional transaction banks share the same entry point: cross-border payments and settlement. The scope of what follows differs materially. GTBs are building a broad stack from the start: treasury and liquidity optimization, digital asset custody, and collateral and margin all register as significant second priorities. For regional transaction banks, the drop after the top two is sharper: it’s the same entry point, with a narrower immediate build.

Digital banks and neobanks are outliers. 24/7 settlement is their highest-ranked priority at 60%. Their competitive differentiation depends on it.

Treasury and liquidity optimization leads for both commercial banks and private banks/ wealth managers at 47% and 40% core strategic priority respectively. Where they diverge is in what follows: commercial banks cluster around cross-border payments and settlement, reflecting a payments and balance-sheet efficiency agenda. Private banks spread almost evenly across every use case, from treasury to client trading to tokenized securities settlement, with no single second priority pulling clear.

Each institution is connecting to the Financial Grid at a different layer. The entry point is different. The destination is the same.

The Build Is Broader Than The Entry Point.

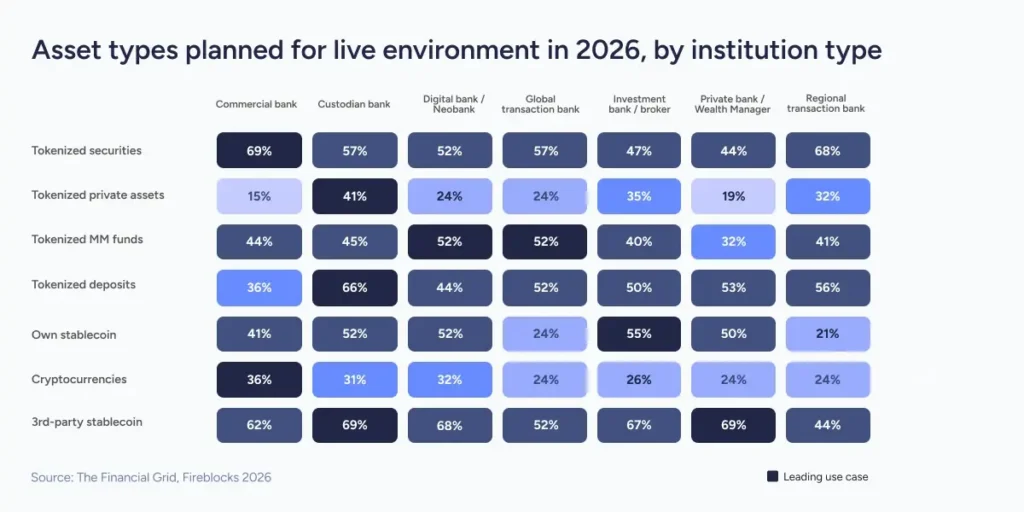

Use case priorities signal intent. Asset type choices confirm it. Across every institution type, financial institutions are not selecting a single instrument to build around. The spread of asset type selection tells a more detailed story than the use case rankings alone.

One finding cuts across every institution type: tokenized securities score high universally, including at institutions whose primary use case is payments. No institution is building for a single asset class.

For payments-focused institutions, the asset type picture is broader than their entry point suggests. Global transaction banks and regional transaction banks both lead with tokenized securities, at 57% and 68% respectively, alongside their cross-border payments priority. The infrastructure being built for payments is the same infrastructure that will support tokenized asset markets when they arrive.

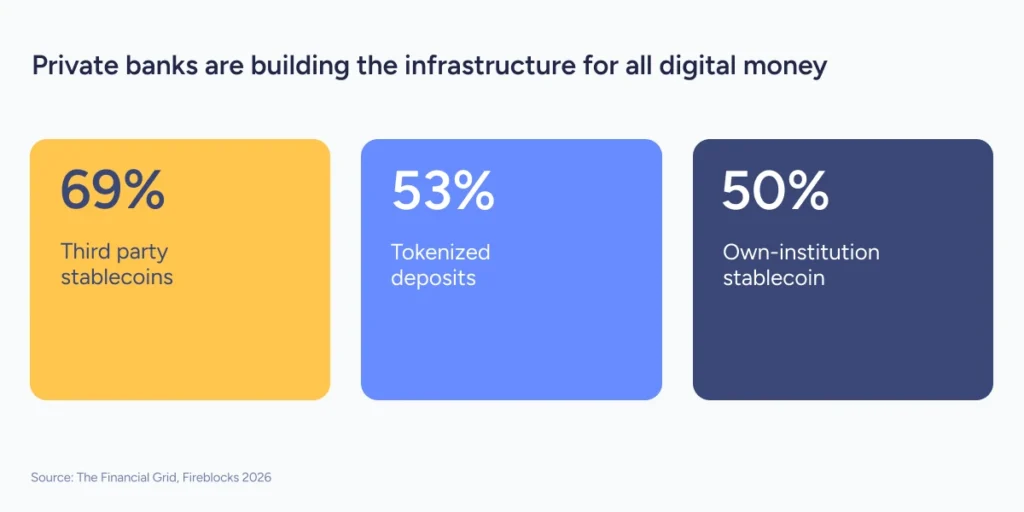

Private banks and wealth managers tell a different story. Third-party stablecoins lead at 69%, tokenized deposits follow at 53%, own-institution issuance comes next at 50%: all three routes are prioritized. These institutions have not chosen a single digital money product; they are building the infrastructure to handle all of them.

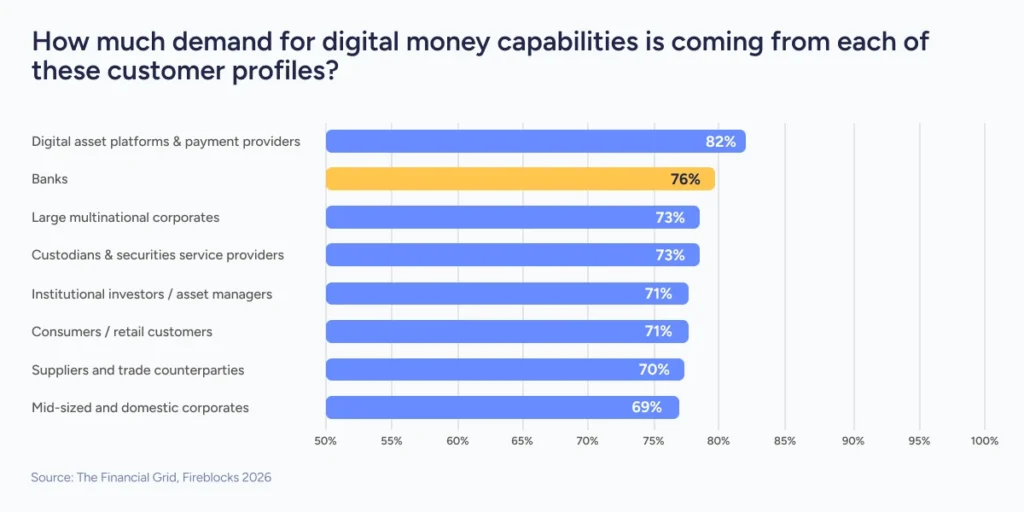

The Biggest Competitive Threat In The Market Is Also Its Biggest Source Of Demand.

Financial institutions are not waiting for client demand to materialize. It is already present, and it is not concentrated in one client type or one segment. Across eight customer profiles surveyed, demand for digital money capabilities is strong or primary at every level. The pressure is coming from all of them simultaneously.

Digital asset platforms and payment providers generate the strongest demand signal in the market. But the more structurally significant finding is that other banks register as the second highest source, with 76% of financial institutions rating them as a strong or primary demand source.

This goes beyond client service. Banks increasingly need their counterparties to have digital asset capabilities in place for settlement, liquidity, and wholesale market operations. A bank building digital asset infrastructure is also building the connectivity its banking counterparties require of it.

The demand is there and the build is funded. What remains is the harder question: how production-ready is digital asset infrastructure?

Part 3: What Production-Ready Actually Requires

Budget commitment and strategic intent are necessary but not sufficient conditions for reaching production. The institutions furthest along in the digital asset build have learned that the constraints are not what they expected: the blockers are mostly internal.

The foundational decisions like custody architecture, wallet infrastructure, skills, and reporting and reconciliation are the ones that determine how fast the investment translates into production capability. And the internal advocates most likely to drive those decisions to resolution are not the ones most institutions would have predicted.

Security And Compliance Are The Unexpected Advocates.

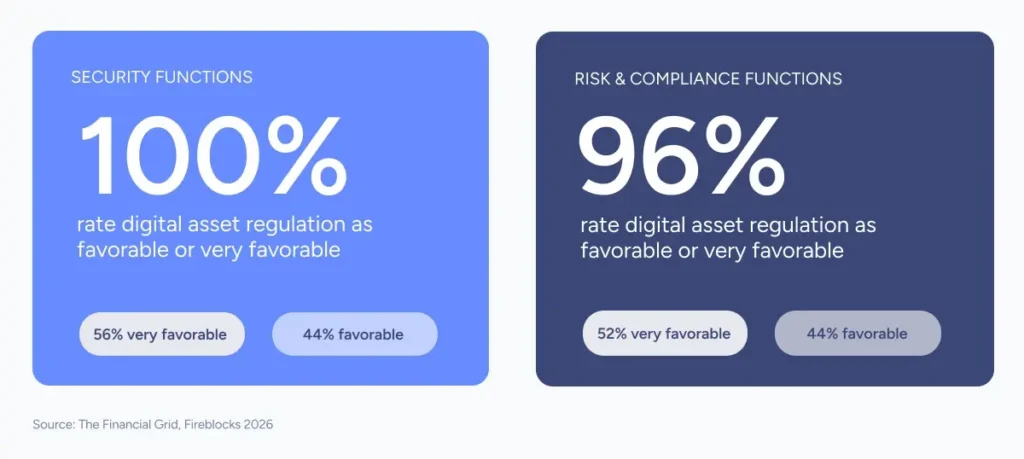

Security functions are leading digital asset initiatives at 30% of financial institutions. Risk and Compliance sits at 22%. Neither is sitting this out: fewer than 2% of either function report being disengaged from the build.

And on regulation, both are more convinced than the C-suite: Security rates it as very favorable at 56%, Risk and Compliance at 52%, against 32% for the C-suite.

Security and compliance functions are optimistic because they understand what production-ready actually requires. MiCA, VARA, OCC clarity, and MAS frameworks are not abstractions to a CISO or a head of financial crime compliance. They are specifications. And specifications, unlike uncertainty, are workable.

The Biggest Obstacle To Scaling Digital Assets Is In-House Expertise.

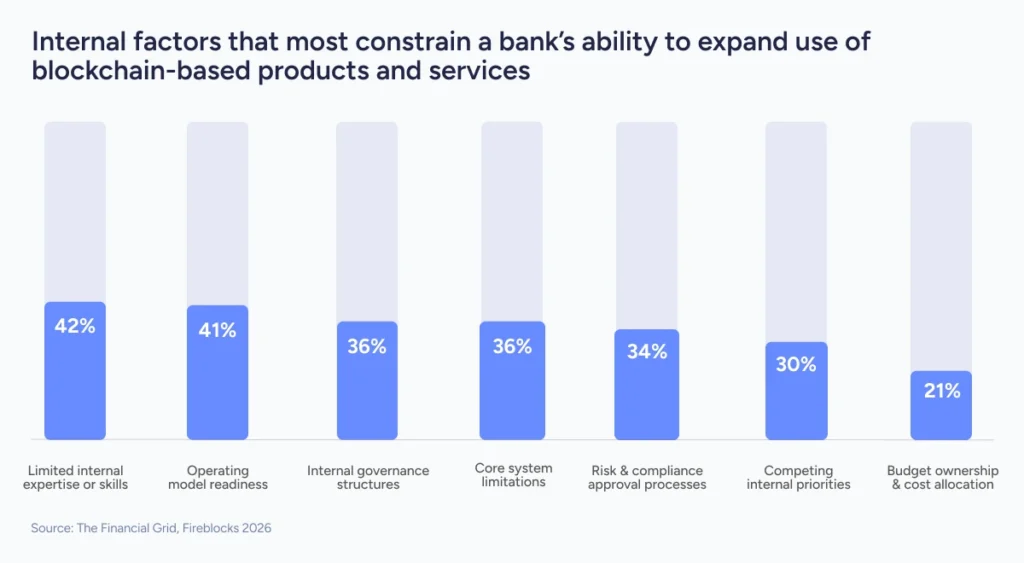

Skills gaps are a blocking obstacle for 42% of financial institutions, the highest of any internal constraint but followed closely by operating model readiness, internal governance structures, core system limitations, and risk and compliance approval processes.

The constraint is not regulatory permission or budget. It is people: the engineers, compliance specialists, and operations staff who can build and run digital asset infrastructure at institutional scale.

The sector breakdown sharpens the picture. Global transaction banks cite skills gaps as a blocking obstacle at 67%, the highest of any sector. Digital banks and neobanks follow at 60%, commercial banks at 54%. The institutions moving fastest on the build are the ones most acutely aware of the talent constraint.

This is why the choice of infrastructure partner is a capability decision. The right partner closes the skills gap through implementation support, production readiness guidance, and operational knowledge built across institutions in multiple markets while reducing reliance on human capital and overhead.

The Custody Decision Is The Foundation For Everything. And 85% Have Not Resolved It.

Only 15% of financial institutions describe their custody and wallet governance infrastructure as fully production-ready. 54% are partially prepared or work in progress. 23% are in early exploration. 8% are not prepared at all.

The custody decision is not one infrastructure choice among many. It is the one that determines the shape of every decision that follows: which digital asset businesses the institution can run, at what scale, and on what timeline. 85% of financial institutions have not yet resolved it.

When financial institutions select a digital asset infrastructure provider, secure institutional custody and wallet governance is rated as the critical factor by 60% of respondents, 14 percentage points ahead of the next criterion.

Wallet Infrastructure Is Where Compliance, Integration, And Security Converge.

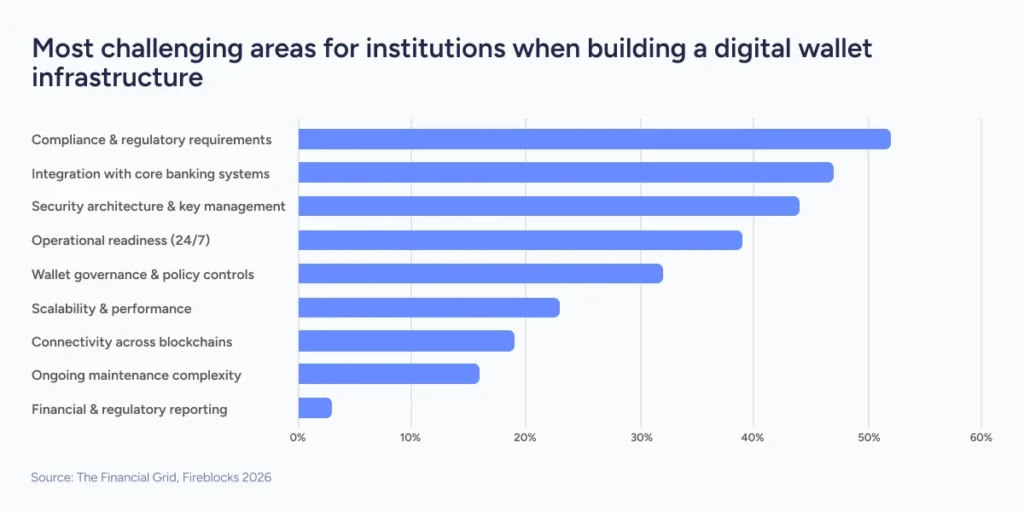

Once the custody architecture decision is made, wallet infrastructure is where production complexity surfaces. Compliance and regulatory requirements lead the wallet build challenges for financial institutions at 52%, followed by integration with core banking and downstream systems at 47%, security architecture and key management at 44%, and operational readiness at 39%.

The four challenges are not separate workstreams. They converge on a single infrastructure decision, at the same moment.

The top four wallet challenges map directly to what institutions rate as critical when selecting an infrastructure provider.

The wallet architecture decision now shapes the product strategy, not the other way around. An institution that chooses wallet infrastructure built for the full range of use cases starts with the architecture that scalability requires. One that does not will face a rebuild or replatforming at the worst possible moment: when it is trying to scale.

The Reporting Blindspot.

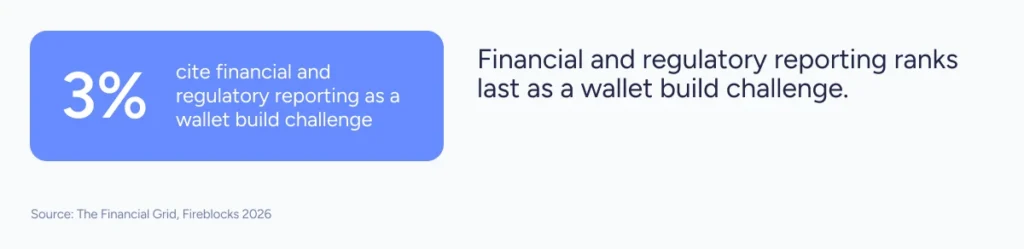

Financial and regulatory reporting for digital assets is cited as a wallet build challenge by only 3% of financial institutions. It ranks last on the list. That figure is almost certainly not a reflection of the challenge itself. It is a reflection of how few institutions have yet encountered it in production.

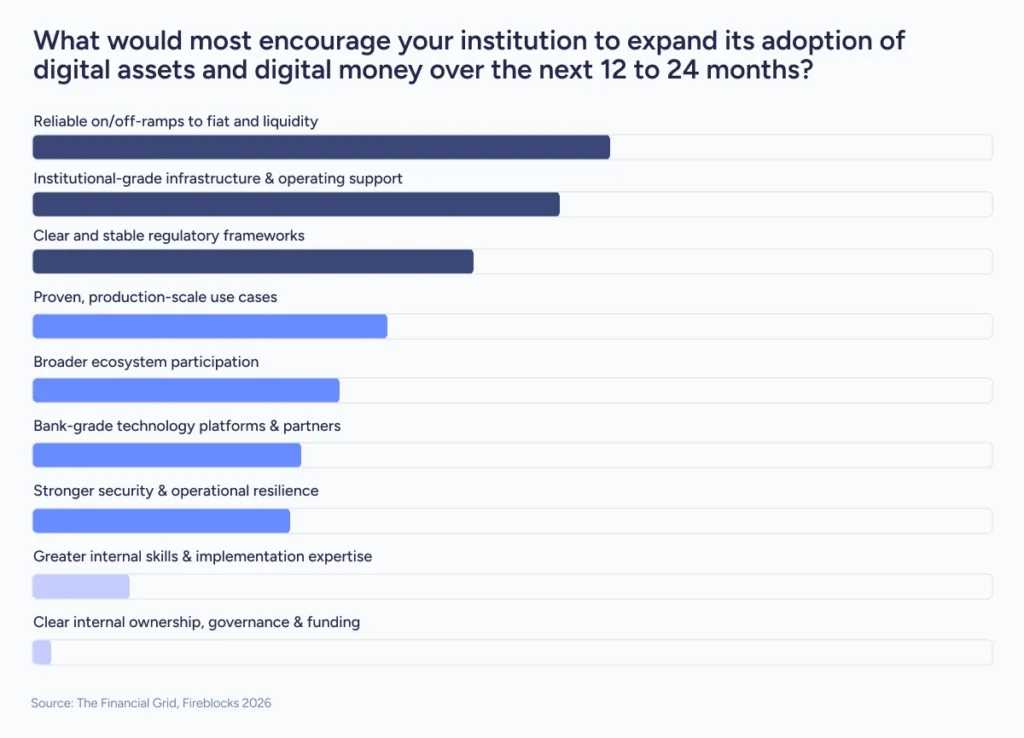

Building Into The Financial Grid.

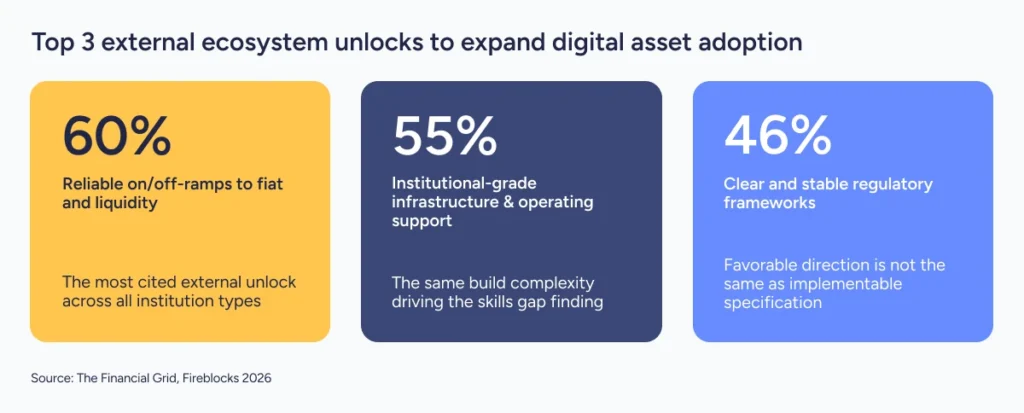

On/off-ramps lead as the factor institutions say would most accelerate their digital asset adoption, but the factors immediately behind them tell the fuller story. 55% cite institutional-grade infrastructure and operating support as a key unlock. 46% cite regulation that is not just favorable in direction but implementable in practice.

Banks need the layers of the Financial Grid to work together: interoperable, coexistent, and functioning.

The internal build is underway and the challenges are understood. Looking externally, banks agree that three factors would accelerate their digital asset adoption.

Conclusion

The global financial system has added new layers before: correspondent banking, card rails, internet banking, mobile. Each time, the institutions that got the infrastructure decisions right early shaped how the next era of finance operated.

Digital assets are that next layer. The Financial Grid is being built now, institution by institution, use case by use case, infrastructure decision by infrastructure decision. The institutions that get those decisions right in 2026 will not just be ready for what comes next. They will be defining it.

Download The Financial Grid here.

Read our buyer’s guide for banks and financial institutions to learn more about key criteria for digital asset infrastructure.

A note on methodology

The findings in this report are based on a number of inputs:

- Primary research conducted globally by the Value Exchange in January 2026 surveying 638 decision makers at financial institutions and corporations across North America, Europe, Latin America, Asia-Pacific, and the Middle East and Africa.

- Our own daily, global experience working with institutions and enterprises integrating stablecoins and digital assets