The Financial Grid is Fireblocks’ 2026 flagship survey report, based on responses from more than 600 C-suite and senior decision-makers at financial institutions and corporates globally. It maps where banks stand in integrating a digital asset layer into the existing financial grid: what they are building, where the build is hard, and how that picture differs by region. The central finding: the decision arc of 2026 has moved on from whether to connect to what kind of connection to build, at which layer, and how fast.

The global report maps each institution connecting to the Financial Grid at a different layer. US institutions have chosen theirs: issuance.

The US Issuance Ambition

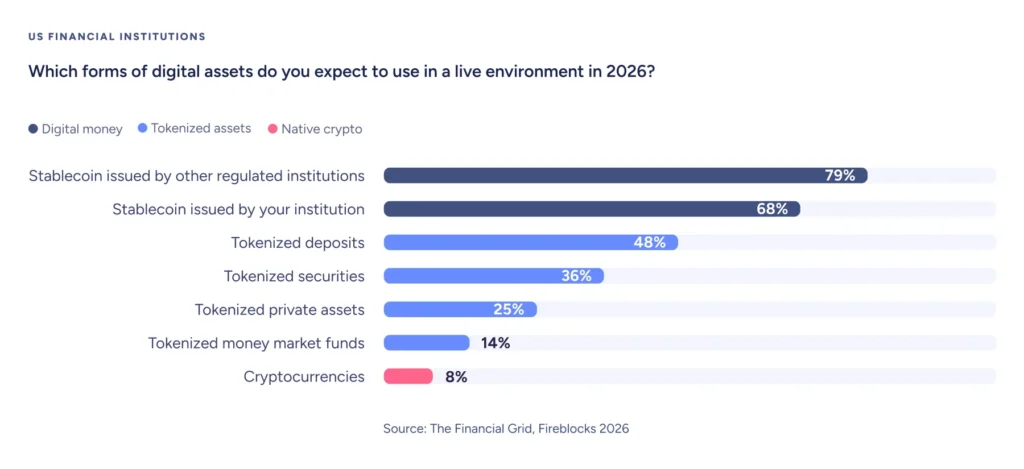

68% of US financial institutions plan to issue their own stablecoins in a live environment, against 16% in APAC and 36% in Europe. While MiCA gave European institutions an established framework for stablecoin issuance, US institutions are now moving toward their own regulatory destination at institutional scale. And 79% plan to deploy stablecoins issued by other regulated institutions alongside their own.

US institutions are building for both sides of the stablecoin market, originating their own and using those issued by other regulated institutions. 79% plan to deploy stablecoins issued by other regulated institutions.

The use cases follow directly from the choice that US institutions have made to connect to the Financial Grid at the issuance layer. 99% rate 24/7 settlement as high or core strategic priority. 90% rate internal settlement using tokenized deposits at the same level.

The entry point is clear. The decision has been made.

US Institutions Are Already Building, Before The Final Rules Land

Connecting to the global Financial Grid’s digital asset infrastructure at the issuance layer requires resolving the layers beneath it first: core systems, operating model, and custody. None of these are issuance-specific decisions, but without them, issuance at scale is not possible.

And US institutions are absorbing that cost now, ahead of the full regulatory specification: 86% have already committed or plan to commit budget in 2026, before CLARITY has passed.

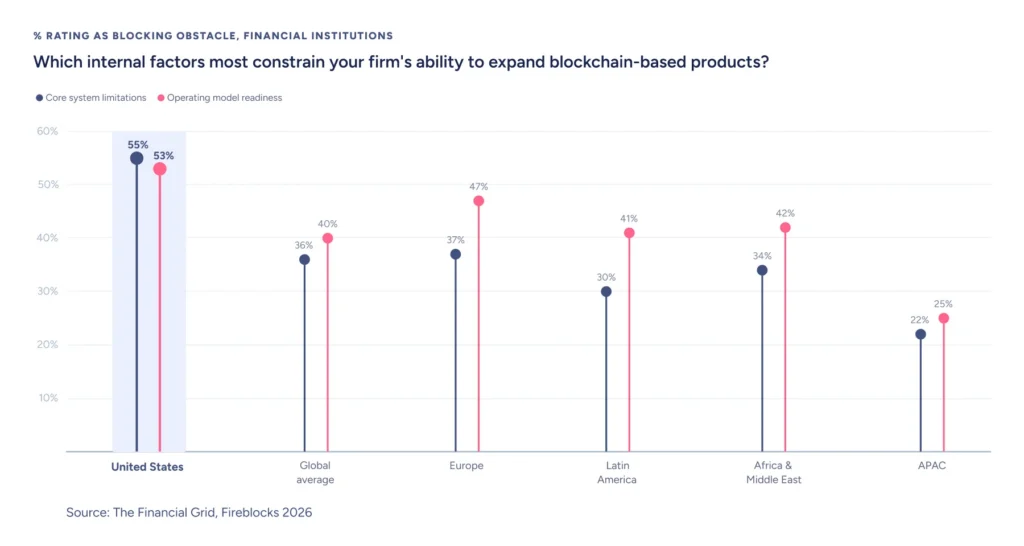

55% identify core system limitations as a blocking obstacle, above the global average. 53% cite operating model readiness as a blocking obstacle, against 40% globally.

Two legislative instruments are key in the United States. GENIUS introduced a national regulatory floor for licensing stablecoin issuers and set standards for both domestic and foreign participants. For banks and other regulated financial institutions, it opened the door to new business and operations using stablecoins for cross-border payments, digital asset settlement, crypto treasury innovation, and more. CLARITY is expected to provide a comprehensive federal market structure framework for digital assets, including around token classification and custody treatment. While 70% cite regulatory uncertainty as a current constraint, 99% expect the direction to be favorable.

As a result, US institutions are doing the infrastructure work that does not require the final regulatory specification—core systems, operating model, custody, waiting for CLARITY before committing to the issuance-specific decisions. 86% have already committed or plan to commit budget to their digital asset build in 2026, even before CLARITY has passed.

Building The Conditions For Digital Asset Scale

The infrastructure work underway now to build custody infrastructure, define the operating model, and integrate into core systems is what positions banks to move at speed when CLARITY lands. The institutions that have resolved these constraints ahead of the specification will face a shorter path to scale production than those that have not.

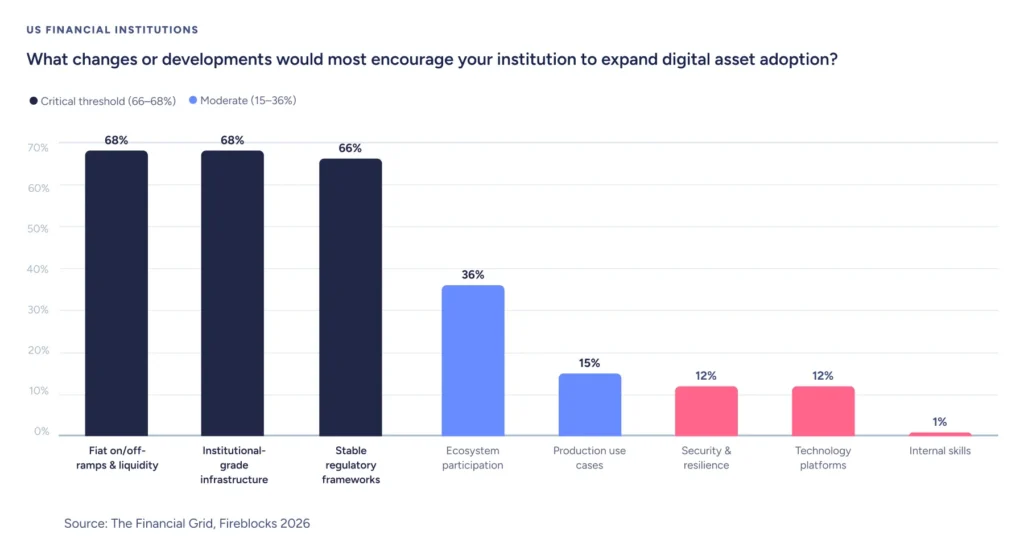

Three factors will determine how well US institutions can sustain that build at scale. All three are entry conditions: without fiat connectivity, operational infrastructure, and a regulatory framework, the first transaction cannot happen. The factors that follow, from ecosystem participation to internal capability, are the conditions for scale once production is live.

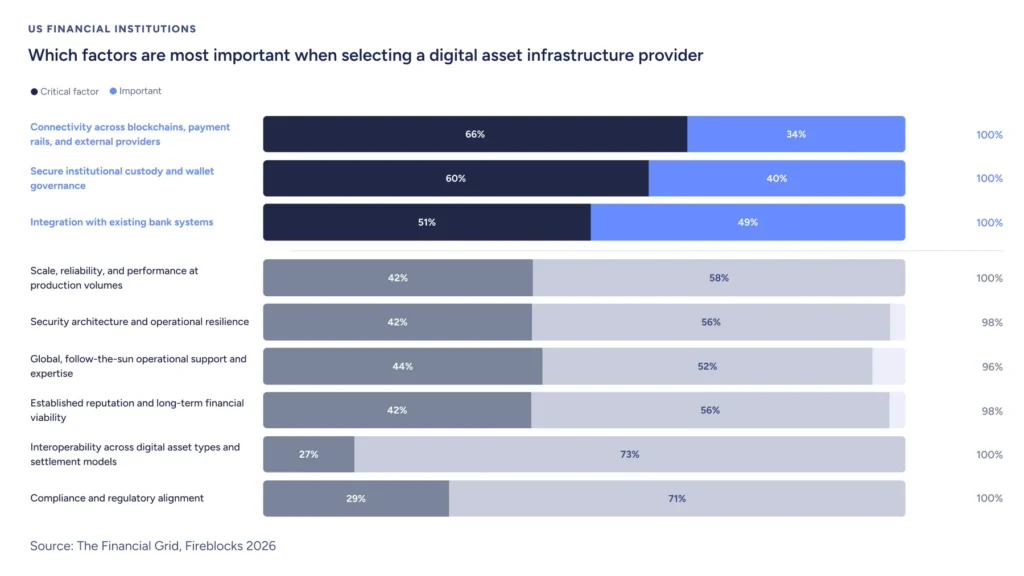

Building that infrastructure is not a solo undertaking. When US institutions select a digital asset infrastructure provider, their criteria reflect their focus on connecting custody, core systems, and payment infrastructure into a single operational layer that will be ready to scale when the regulatory framework is clarified. Connectivity across blockchains, payment rails, and external providers leads as a critical factor at 66%, followed by secure institutional custody and wallet governance at 60% and integration with existing bank systems at 51%.

Across every factor, the expectation is the same: full-stack delivery, not point solutions. US institutions are not selecting for a single capability, they are selecting for a provider that can deliver across the entire stack.

The institutions getting the infrastructure decisions right in 2026 will not just be ready for what comes next. They will be defining it.

Read the flagship Financial Grid report for more insights and global data from Fireblocks’ 2026 survey.

Read our wallet infrastructure blueprint for banks to learn more about key criteria for digital asset infrastructure.

Download the pdf version of the Financial Grid USA.