The Financial Grid is Fireblocks’ 2026 flagship survey report, based on responses from more than 600 C-suite and senior decision-makers at financial institutions and corporates globally. It maps where banks stand in integrating a digital asset layer into the existing financial grid: what they are building, where the build is hard, and how that picture differs by region.

88% of financial institutions have committed or will commit budget to digital asset infrastructure in 2026. Only 16% have reached production. That gap between production-scale spending and production-scale capability is the central finding of The Financial Grid.

The global report maps each institution connecting to the Financial Grid at a different layer. In Latin America, the digital asset infrastructure build is underway. The data maps where it is moving, and where the work remains.

Latin America Has Funded Its Digital Asset Build And Begun The Work

41% of Latin American financial institutions had already committed budget for digital asset infrastructure before 2026 began, twice the rate of US institutions at 21%, and above North America overall at 27% and Africa and the Middle East at 40%. Latin America trails APAC at 62% and Europe at 50%.

A further 50% however are committing investments in 2026. Among the three largest Latin American markets in the survey, Argentina stands out: 58% of Argentine institutions had already committed budget before 2026 began, against 34% in Brazil and 31% in Mexico.

The scale of that commitment is where the data becomes distinctive. 50% of Latin American institutions are investing $1 million or more in their digital asset infrastructure build over the next 12 months. In the United States, that figure is 15%. Both regions share the same modal investment band. The distribution above it looks nothing alike.

The investment scale reflects a strategic conviction that runs across every measure in the data. 75% of Latin American institutions cite transformation of financial infrastructure as a significant strategic driver of their digital asset investment, the highest of any region globally. 93% expect the regulatory environment to be favorable or very favorable. The capital is committed, the strategic case is settled, and the build is underway.

Pilot to Production: The Governance and Security Gap

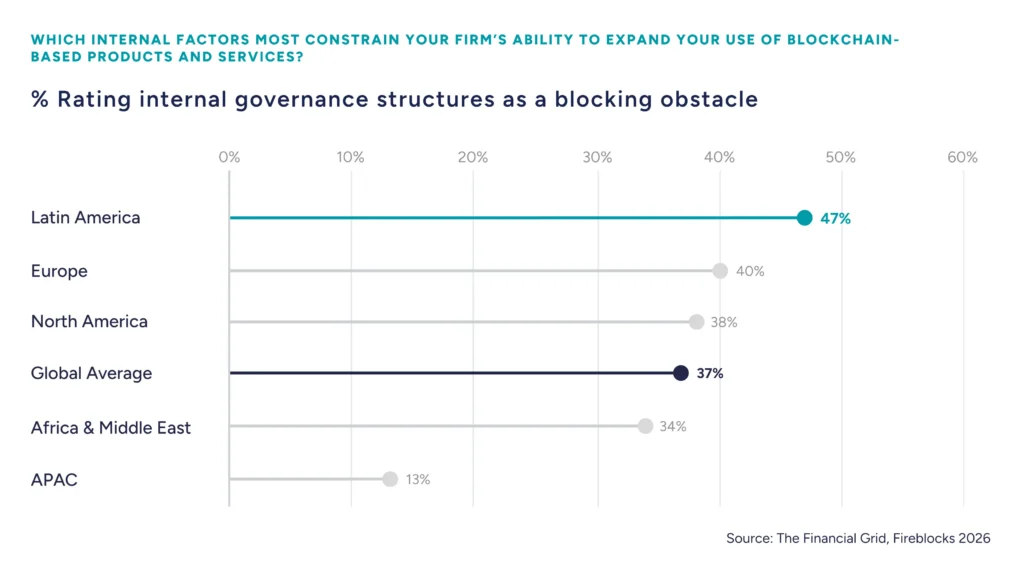

50% of Latin American financial institutions are in active pilots for digital assets, internal or external. 14% are in production. The gap between the two is explained by what is happening inside institutions and around them simultaneously.

Internal governance structures are the top internal constraint, cited as a blocking obstacle by 47% of Latin American institutions, the highest of any region globally and 10 percentage points above the global figure. And Mexico records the highest internal governance blocking rate of any country globally at 71%.

Across the region, budget ownership and cost allocation ranks last among all internal constraints at 15%, far below any other internal factor.

Latin America’s Full Stack Digital Asset Ambition

Latin American financial institutions are building toward the same use case priorities as the global average. 92% rate 24/7 settlement and real-time payments as a high or core strategic priority, cross-border payments and digital asset custody both at 83%.

The asset type priorities follow the same order as the global average and at broadly similar levels: third-party stablecoins lead at 63%, tokenized deposits at 57%, tokenized securities at 54%, own-institution stablecoin issuance at 47%.

Where Latin America diverges from the global picture is in the infrastructure ambition behind those priorities.

Both figures are the highest of any region globally. Latin America’s institutions have set their sights on the full infrastructure stack: the issuance capability, the FMI connectivity, and the digital asset infrastructure that make a broad range of asset types operable at scale.

Custody Is Where Latin America’s Build Becomes Production Ready

When asked what would most accelerate their digital asset build, Latin American institutions point directly to the infrastructure layer. Institutional-grade infrastructure and operational support leads at 59%, followed by fiat on/off-ramps at 51%. Proven production-scale use cases follow at 41%.

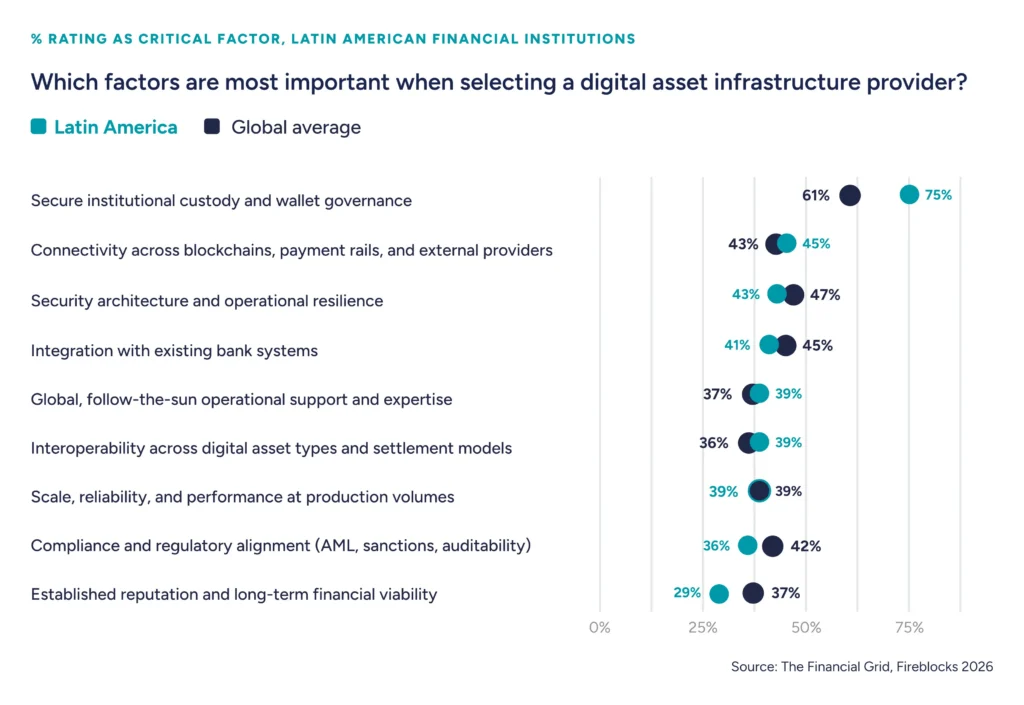

The choice of infrastructure provider is where that intent becomes a decision. When Latin American institutions select a digital asset infrastructure provider, secure institutional custody and wallet governance leads as a critical factor at 75%, the highest of any region globally and 13 percentage points above the global figure of 61%.

The custody figure connects directly to the governance story. The constraint holding institutions back from production is organisational: governance structures, operating model readiness, compliance processes. Custody infrastructure is where those organisational decisions get resolved.

The custody decision is not one infrastructure choice among many. It is the one that determines the shape of every decision that follows: which digital asset businesses the institution can run, at what scale, and on what timeline. When Latin America gets the custody build right, its institutions will be ready to operate the full range of digital asset businesses they have already committed to building.

Read the flagship Financial Grid report for more insights and global data from Fireblocks’ 2026 survey.

Read The Financial Grid USA for insights on US financial institutions’ survey results. For Asia Pacific bank insights, read The Financial Grid APAC. Read The Financial Grid Europe & The UK.

Read our wallet infrastructure blueprint for banks to learn more about key criteria for digital asset infrastructure.

Download The Financial Grid Latin America here.