Introduction: Beyond Payment Rails

You’ve transformed your treasury operations and enabled receiver wallets (i.e. stablecoin payment accounts) with stablecoin infrastructure. You’ve optimized capital efficiency, eliminated prefunding lag, achieved real-time settlement, and are generating new revenue streams by creating new customer relationships. But here’s the strategic inflection point most remittance operators miss: the non-custodial wallet infrastructure you deployed for operational efficiency in your treasury and for receiver wallet creation is simultaneously a platform for creating long-term customer value. This is the opportunity to become deeply embedded as a core part of your customers’ financial ecosystem.

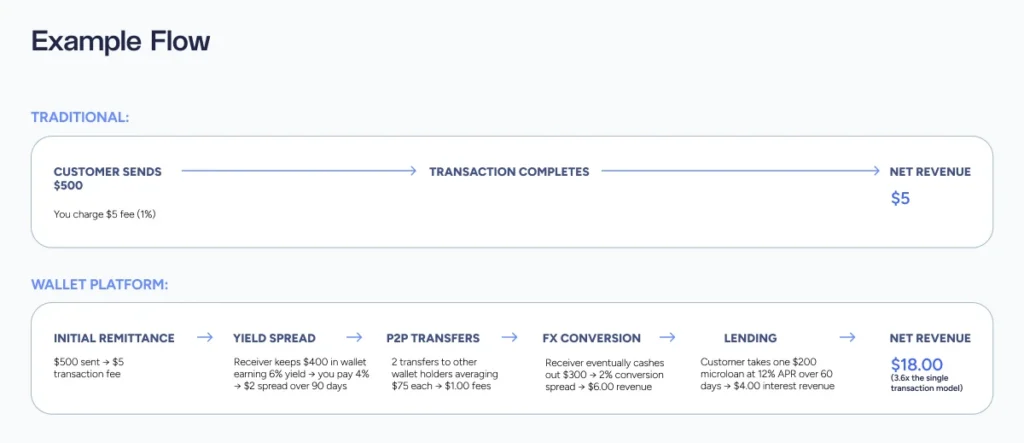

With embedded wallets infrastructure, the same receiver customer who sends a remittance can hold balances, pay bills, earn yield, access credit, and conduct P2P transactions. These all generate revenue from a single acquisition. Your cost to acquire a customer gets amortized across multiple revenue streams over an extended relationship rather than a single transaction fee.

As outlined in our receiver wallets blueprint, remittance providers who embrace wallet-based services can capture at least 2x more revenue per customer than transaction-only competitors while simultaneously increasing customer retention and reducing churn.

This blueprint provides a practical implementation guide for offering new financial services via stablecoin wallets.

Use Case: Offer New Financial Services

Grow and Scale: Tap Into New Revenue Streams, Customer Retention and Expansion

The opportunity: now that you have the infrastructure in place to support stablecoin remittances and receiver wallet accounts (including access to staking and yield), you can expand your platform and use cases to:

- meet customer demand

- open new revenue streams

- offer entirely new financial products and services

- maintain a competitive edge

Risk Management and Safeguarding Expansion

Regulatory compliance is non-negotiable: Note that each new product outlined below triggers additional regulatory requirements. For that reason, it is advised to start with pilot markets instead of launching all services in all markets simultaneously. Identify 2-3 jurisdictions with favorable regulatory environments and strong remittance corridors. Prove the operational model, refine the economics, and develop best practices before expanding to additional markets.

Transaction monitoring and compliance: Expand your existing digital asset compliance infrastructure to handle consumer transaction monitoring, suspicious activity reporting, and travel rule compliance for customer-facing services. Your treasury operations already have baseline compliance tooling; extend this to consumer-scale transaction volumes with appropriate automation.

A Step-By-Step Expansion Blueprint

Step 1: Launch Stablecoin-Denominated Savings Products

Capture storage revenue: Once customers hold balances in wallets, you have an opportunity to generate yield on those balances and share a portion with customers as savings interest, keeping the spread as revenue. Remittance providers can enable goal-based savings, automated rules, e.g. “save 10% of each remittance,” and round-up features to further increase customer engagement and retention.

The mechanics:

- Yield generation: Deploy customer funds held in stablecoin balances into yield-generating DeFi protocols, tokenized money market funds, or partner arrangements with institutional crypto lenders. Current yields on stablecoin deposits range from 4-8% APY depending on market conditions and risk tolerance.

- Revenue model: If you generate 6% yield on customer balances and pay customers 4%, you keep the 2% spread as storage revenue. On $10M in customer balances, that’s $200K annual revenue with minimal operational overhead.

- Risk management: Structure savings products with appropriate risk tiers. Conservative customers get lower yields backed by institutional-grade money market funds. Risk-tolerant customers access higher yields with appropriate disclosures about DeFi protocol risks.

Regulatory framework: Savings products may trigger banking or securities regulations depending on jurisdiction and structure. Work with legal counsel to determine whether you’re offering bank-like deposit accounts, money market fund equivalents, or other structures, and ensure appropriate licensing and consumer protection compliance.

Customer benefit: For receivers in high-inflation economies, stablecoin savings products provide access to USD-denominated savings earning positive real returns. This can be a transformative financial service for populations with limited access to stable-value savings vehicles.

Technical Requirements

Yield generation strategy: Decide whether to generate yield through DeFi protocols (Aave, Morpho), tokenized treasury products (OUSG, BUIDL), or institutional lending counterparties. Each approach has different risk profiles, regulatory considerations, and operational complexity. Start with the most conservative option (tokenized treasuries) and expand to higher-yield strategies as you gain operational confidence.

Note that savings products might trigger banking or securities regulations, and yield risk should be managed appropriately. If you offer savings products backed by DeFi yields or crypto lending, understand that yields fluctuate and counterparty risk exists. Structure products with appropriate risk disclosures, maintain reserves to smooth yield volatility, and never promise fixed returns you cannot guarantee. Better to offer conservative yields you can reliably deliver than aggressive returns that create reputational risk when market conditions change.

Step 2: Enable P2P Transfers Between Wallet Holders

Network effects begin here: When you enable instant, free (or low-cost) P2P transfers between your wallet holders, you transform from a remittance provider into a payment network. Each additional wallet holder increases the utility of the platform for all existing users. This creates network effects where every wallet holder becomes a potential sender and receiver.

Technical implementation: P2P transfers are simple from an infrastructure perspective, with value moving between stablecoin payment accounts you control on the same wallet infrastructure. No on/off-ramps required, no correspondent banking, no FX conversion needed if both parties hold stablecoins.

Operational advantages:

- Instant settlement: Transfers complete in seconds because they’re entirely onchain movements between wallets you manage.

- Minimal cost: Transaction fees measured in cents, not dollars.

- Real-time confirmation: Both sender and receiver see the transfer immediately.

- Instant reconciliation: All transactions recorded onchain with complete auditability.

Monetization approach:

- Option 1: Charge a small fixed fee per transfer (e.g., $0.25-$0.50)

- Option 2: Offer free P2P transfers as a customer acquisition tool, monetizing through FX conversion when users eventually cash out

- Option 3: Tiered model—free for small amounts/up to X transfers per month, then small fees for larger transfers/additional volume

Growth strategy: P2P functionality drives organic adoption. When a wallet holder sends money P2P to someone without a wallet, that creates a natural onboarding opportunity. The receiver must create a wallet to claim the funds, further expanding your network through user behavior rather than marketing spend.

Note that customer funds should always be protected rigorously. Customer wallet balances are customer property. Implement segregated account structures, regular attestations, and clear terms of service that define your custody responsibilities. Consider insurance products that protect customer funds from operational failures, cyber incidents, or other risks. Customer trust is foundational to wallet adoption.

Step 3: Introduce Lending and Credit Products

Unlock the highest-margin revenue stream: Lending products backed by stablecoin collateral represent the most lucrative expansion opportunity for remittance providers with wallet infrastructure. Interest rate spreads of 8-15% are standard, and stablecoin collateralization dramatically reduces default risk. Use stablecoin wallet balances and transaction history as the basis for credit products. Microloans secured by stablecoin collateral or credit lines based on remittance flow patterns are all made possible.

Product structure options

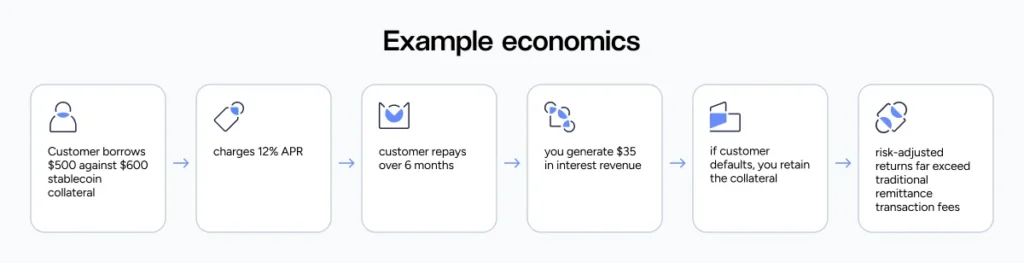

Collateralized loans: Customers borrow against stablecoin balances held in their wallet. If a customer holds $1,000 USDC, they can borrow up to $800 (80% LTV) immediately. If they fail to repay, you simply retain the collateral. Default risk is minimized because the collateral is already in your custody.

Flow-based credit: For customers with consistent remittance receipt patterns, offer unsecured credit lines based on historical transaction data. Someone who receives $500 monthly could access a $200 credit line that automatically repays from incoming remittances. You have visibility into their cash flow, making underwriting straightforward.

Sender-backed credit: Enable senders to provide credit guarantees for receivers. A sender in the US guarantees loan repayment for their family member in the Philippines by committing future remittances as collateral. This model combines the trust relationships inherent in remittance flows with formal credit products.

Implementation considerations:

- Loan management system: Build or integrate a loan origination and servicing platform that connects with your wallet infrastructure. Track balances, calculate interest, manage repayment schedules, and handle collections.

- Credit scoring: Develop underwriting models based on remittance transaction history, wallet balance patterns, bill payment reliability, and P2P activity. The data you collect from wallet usage provides far richer credit signals than traditional credit bureaus have access to in many emerging markets.

- Regulatory compliance: Lending triggers consumer finance regulations. Ensure you have appropriate lending licenses, truth-in-lending disclosures, interest rate cap compliance, and collections procedures that meet local regulatory requirements.

Lending income can be earned on interest rate spreads and origination fees on loans extended to wallet users.

Technical Requirements

Loan management system: Build or license loan origination, servicing, and collections capabilities. This can be a custom-built system integrated with your wallet platform or a licensed SaaS product (e.g., from modern lending infrastructure providers). The key requirement is tight integration with your wallet infrastructure so loan disbursement, repayment, and collateral management happen automatically.

Note that lending requires consumer finance compliance. Lending products introduce credit risk that transaction-only remittance doesn’t carry. Implement robust underwriting standards, start with conservative loan-to-value ratios for collateralized lending, and use flow-based credit cautiously. Your transaction data provides strong credit signals, but validate your models with real performance data before scaling lending operations aggressively.

Participate in crypto beyond stablecoins

Once receiver wallets are set up and customers have adopted stablecoins, there are many other DeFi use cases and revenue streams that can be turned on in addition to lending and credit. One example is swaps and staking.

Stablecoins held in receiver wallets can be swapped for virtually any other crypto or digital asset, for example ETH. Receiver customers can then stake that ETH to earn rewards. The revenue opportunity lies in taking a percentage cut of the swap and/or of the staking rewards similar to the lending interest.

Ecosystem Value vs. Price-Only Competition

Example of the new competitive moat powered by stablecoin wallets

Sample Success Metrics: Measuring Platform Performance

Traditional remittance KPIs remain relevant: Transaction volume, average transaction value, customer acquisition cost, and fee revenue per transaction still matter. However, wallet platforms require additional metrics that capture multi-product engagement and customer lifetime value.

Essential wallet platform metrics

Wallet adoption rate: Percentage of remittance receivers who retain balances in wallets versus immediately cashing out.

Multi-product usage: Percentage of wallet holders who use 2+ services, e.g. remittance + savings.

Average balance per wallet: Total stablecoin balances divided by number of active wallet holders. This directly drives storage revenue and lending opportunities.

Revenue per customer: Total revenue (transaction fees + storage revenue + conversion revenue + lending interest) divided by active customers. Compare wallet platform customers to transaction-only customers.

Customer lifetime value (LTV): Model expected revenue from a customer over their relationship with your platform based on engagement patterns and product usage. Wallet customers should show dramatically higher LTV than transaction-only users.

Retention rate: Measure retention for wallet customers versus transaction-only customers.

Savings product adoption: Percentage of wallet holders with non-zero savings balances earning yield.

Lending attachment rate: Percentage of wallet holders who take loans for collateralized lending and flow-based credit products.

Summary: Requirements for Offering New Financial Services

Expanding from remittance transactions to comprehensive financial services requires infrastructure that supports P2P transfers, savings products, DeFi and lending while maintaining regulatory compliance and operational simplicity.

- P2P Transfer Capabilities: Enable instant, low-cost transfers between wallet holders entirely onchain with settlement in seconds and minimal transaction costs. Since transfers occur between stablecoin payment accounts on your infrastructure, no on/off-ramps or FX conversion is required. Real-time reconciliation and complete onchain auditability simplify compliance while creating network effects where every wallet holder becomes both sender and receiver.

- Savings and Yield Products: Deploy customer stablecoin balances into yield-generating opportunities through integrations with DeFi protocols, tokenized money market funds (OUSG, BUIDL), and institutional crypto lending partners. Start with conservative tokenized treasury products, then expand to higher-yield strategies as operational confidence builds.

- Lending and Credit Infrastructure: Offer collateralized loans against stablecoin wallet balances, flow-based credit lines based on remittance transaction history, or sender-backed credit products. Wallet infrastructure enables automatic loan disbursement, repayment tracking, and collateral management with tight integration between lending systems and custody.

- Enhanced Compliance and Monitoring: Extend existing treasury compliance infrastructure to consumer-scale transaction volumes with automated consumer KYC/AML, suspicious activity reporting, and Travel Rule compliance for customer-facing services. Integrations with Notabene, Elliptic, and Chainalysis handle transaction monitoring across bill payments, P2P transfers, savings products, and lending operations.

- Mobile Application Layer: Extend existing customer-facing mobile apps to include wallet balance viewing, P2P transfer functionality, savings product management, and loan applications. The backend wallet infrastructure handles core logic while you build the customer experience layer optimized for your brand and market needs.

- Risk Management and Safeguarding: Implement segregated account structures, regular attestations, and clear custody terms for customer wallet balances. MPC-based security architecture with hardware isolation protects customer funds while maintaining operational flexibility.

- Operational Simplicity at Scale: The same security model, policy engine, and operational workflows managing treasury operations extend to consumer financial services without architectural changes. Real-time balance tracking, comprehensive transaction history, and API access integrate with existing accounting and ERP systems. All transactions recorded onchain provide complete auditability, making reconciliation significantly simpler than traditional financial systems managing multiple product lines.

By following the steps outlined in all three remittances blueprints, you’re ready to transform your entire business model by owning both ends of a transaction (sender + receiver relationship); tapping into multiple revenue streams per customer; understanding customer data, flow patterns and behavioral insights; lowering CAC; and gaining more ecosystem value vs. price-only competition. Stablecoins for remittances offer comprehensive financial services platforms that drive customer retention and revenue expansion.

Request a demo to discuss your stablecoin strategy with our payments experts today.