The global financial system is in flux. The relentless pace of innovation, fuelled by the rise of digital assets, is causing a seismic shift. As this change reshapes the landscape, the question increasingly asked by banks and other financial institutions is not if they will be affected, but how they will adapt to the powerful forces of tokenization.

At Fireblocks, a front-row seat to this transformation has allowed us to help over 2,400 businesses securely issue, custody, and transfer tokenized money, tokenized assets and cryptocurrencies. We are seeing first hand how a new form of money is emerging.

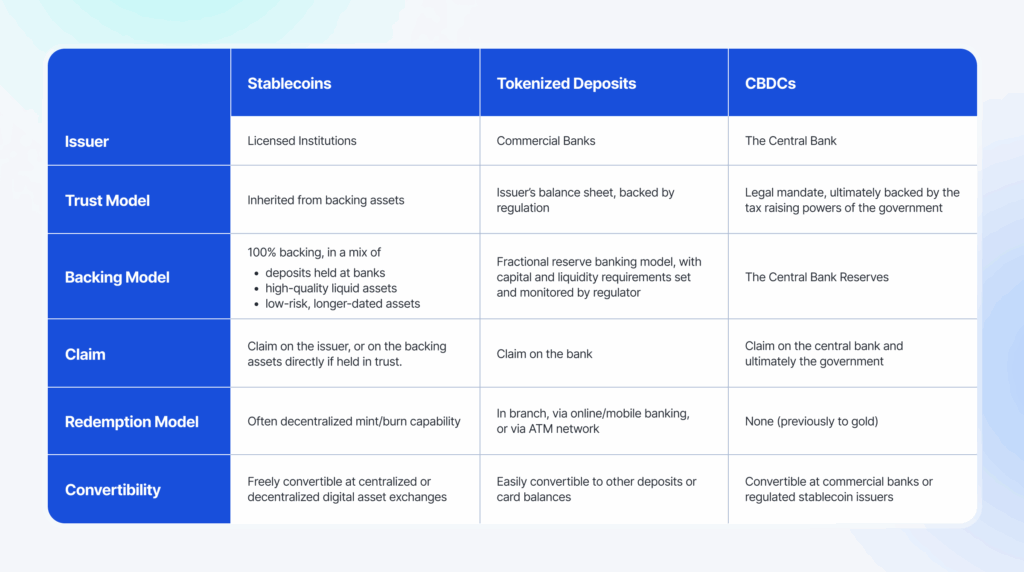

Stablecoins, tokenized deposits, and central bank digital currencies (CBDCs) represent three distinct approaches to digital money. Each carries its own implications for regulation, trust, and market infrastructure.

Understanding Digital Money: A Framework

To understand these new forms of money, it helps to view them through three lenses: the issuer, the inherent trust model, and the underlying backing model.

The table below summarizes how stablecoins, tokenized deposits, and CBDCs differ across these three foundational dimensions:

The issuer

- A non-regulated stablecoin can be issued by almost anyone, from a tech company to a major financial institution. The permitted issuers of regulated stablecoins differ by jurisdiction, but are most commonly a licensed financial institution.

- A tokenized deposit can originate from a regulated commercial bank or depository institution.

- A CBDC can be issued only by a central bank.

The trust and backing models

All of these forms of money carry an element of credit risk. Stablecoin issuers mitigate this by demonstrating that their digital currency is fully backed by high quality assets, thereby inheriting trust. And they manage liquidity risk by holding a mix of highly liquid and longer-dated assets. Commercial banks, with their centuries-old fractional reserve model, offer an established trust framework backed by strict regulatory oversight. Central bank money, however, stands as the ultimate “risk-free” benchmark. Its trust comes from the central bank’s unique legal mandate as the state’s sole issuer of currency, strengthened by the government’s ability to levy taxes across the economy.

At Sibos 2025, Federal Reserve Governor Waller reminded us that different types of money already coexist seamlessly. Retail customers use banknotes (central bank money), bank deposits (commercial bank money), and e-money. And they use credit and debit cards without worrying about the underlying differences.

The digital money ecosystem functions in the same way, with stablecoins, tokenized deposits, and CBDCs each serving a slightly different purpose. The key is ensuring what is known as the singleness of money — their full interchangeability at par value — to ensure frictionless, trusted interactions, just as we expect today.

The Rise of Stablecoins

The rise of stablecoins has been meteoric. In just the past year, their circulating supply has soared from $165 billion to $310 billion. They excel as bearer assets that flow freely across borders, enabling instant and vastly more efficient cross-border payments. This is a stark contrast to the slow, costly, and often cumbersome chains of correspondent banks in certain corridors of the traditional system. Critically, required international controls that act to prevent anti-money laundering and counter terrorist financing can be equally implemented for stablecoin transfers as they are for fiat movements between banks.

Accessibility is a key advantage: anyone with a digital asset wallet can hold them, democratizing access to financial services without the need for a traditional bank account. Despite not offering yield to holders, the market has embraced them: Tether’s USDT dominates with over $176 billion in circulating supply, while Circle’s USDC has reached $74 billion, cementing their place at the foundation of this evolving financial landscape.

What is a Tokenized Deposit?

A tokenized deposit is simply an onchain representation of a traditional bank deposit. This means it can only be held by customers who have gone through the bank’s standard onboarding and KYC processes.

Unlike most stablecoins, tokenized deposits can pay interest and, due to their underlying fractional reserve model, are far more capital-efficient for banks. However, it’s crucial to remember that a tokenized deposit is a direct claim on the issuing bank, with all the associated risks—a reality that former customers of Silicon Valley Bank and Credit Suisse understand all too well.

The banking industry is already putting this into practice. Citi Token Services and JP Morgan’s Kinexys Digital Payments are examples of major institutions using tokenized deposits to enable real-time liquidity and payments across multiple jurisdictions, with the latter now processing billions of dollars in daily transactions for its clients.

How do CBDCs fit in?

Central bank money stands as the ultimate “risk-free” asset. While no asset is entirely without risk, a government’s ability to levy taxes and issue its own currency via the central bank makes its money more reliable than that of a commercial bank in the same country.

Many argue that the existence of a freely exchangeable retail CBDC will help ensure the singleness of money. So it’s no surprise that roughly 90% of the world’s central banks are exploring one. Yet the path forward remains uneven: in markets like the US, political opposition and concerns around privacy, surveillance, and the role of government in retail finance have effectively paused CBDC development. Leading central banks are confronting this head-on, building in privacy by design, but a wider public discourse is needed to ensure citizens understand the legal safeguards in place and have a say in how they want to interact with the central bank in the future.

In the meantime, projects continue elsewhere. One such example is that of Project Acacia, where the Reserve Bank of Australia is actively developing and testing prototypes of CBDCs and other forms of digital currency in partnership with the Digital Finance Cooperative Research Centre.

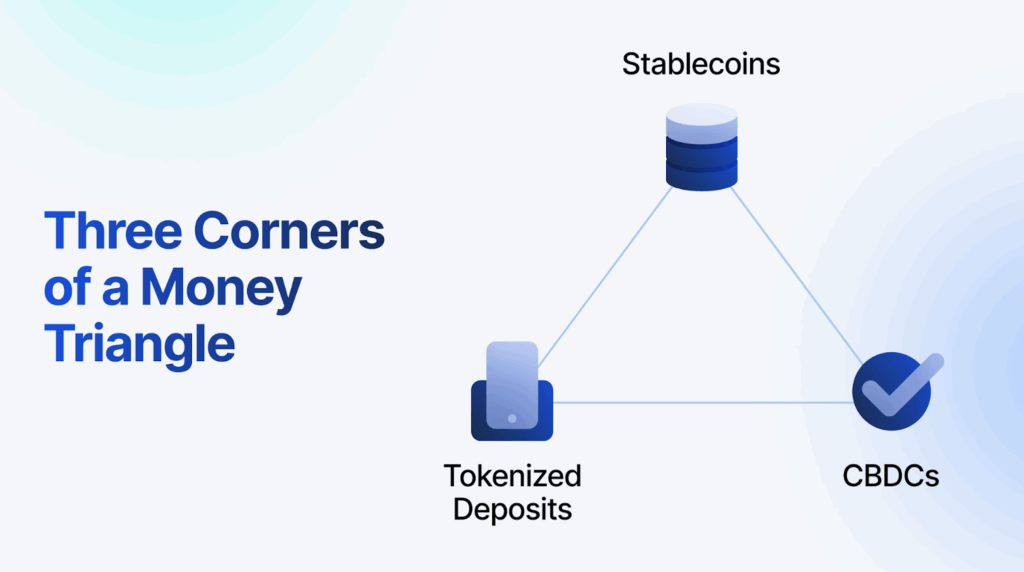

Three Corners of the Same Triangle

Ultimately, we need to stop thinking about these three forms of money as competitors. As the system matures, it’s clear they will co-exist as three corners of a new digital money triangle, just as different forms of money do today.

- CBDCs comprise two forms:

- A retail CBDC is for use by the general public, functioning as a digital form of cash for everyday consumption. Retail CBDCs can provide a monetary anchor, ensuring other forms of money do not deviate from par value.

- A wholesale CBDC is specifically for use among financial institutions, serving as a mechanism for interbank transactions and settlement. They can provide a risk-free settlement asset for wholesale markets and between the other forms of money.

- Tokenized deposits allow banks to continue intermediating between borrowers and savers, providing credit to support economic growth.

- And stablecoins enable more efficient and programmable payment capabilities that are unconstrained by the boundaries of a single bank or country.

A thriving digital asset ecosystem requires all three.

The Importance of Interoperability

In a world of diverse forms of money, with different governance and operating models, interoperability becomes critically important. It ensures that stablecoins, tokenized deposits, and CBDCs can work together seamlessly. Without it, we risk creating isolated financial silos that recreate the very friction we are trying to reduce.

That interoperability will help to unlock the power of programmability and composability on blockchains.This will allow us, for example, to program a tokenised deposit to move funds instantly to the merchant at the moment goods are delivered, while allowing the delivery driver to simultaneously receive their fee in a stablecoin of their choosing, and programmatically pay what is owed to the tax office in the form of a CBDC in real-time, all while eliminating the need for manual reconciliation.

How adoption is playing out

At Fireblocks, we are seeing banks taking their first steps into digital money in similar ways, but with clear leaders. Generally speaking, stablecoins are the front runner due to ease of adoption, followed by tokenized deposits, and finally CBDCs in more beginning stages (with aforementioned stalls, starts and stops along the way).

According to EY’s latest report, institutions are anticipating that stablecoins will account for over 5% of global payments by 2030. Just as a bank’s clients are used to multi-currency accounts today, we believe multi-currency stablecoin banking will be a standard feature within a handful of years. Account holders will see balances in USD, EUR next to their USDC or EURI balances, and will be able to receive, hold balances and make compliant outbound payments using a set of stablecoins pegged to multiple currencies. Banks will also earn fees onboarding and offboarding these stablecoins to fiat currencies.

Likewise, treasury departments are adopting stablecoins to add resilience to their existing nostro-vostro banking practices. Providing a secondary, but crucially real-time, rail ensures that unfunded nostros and missed payments can be avoided.

Tokenized deposits provide immediate value to the treasury departments and customers of multi-jurisdictional commercial banks, allowing them to move money between international entities in real time without the uncertainty around delivery timelines and the fees associated with correspondent banking.

These are just three examples of how forward-looking banks are adopting digital money with tangible benefits that enable them to provide differentiated services to their clients today.

The ability to provide real-time banking services with digital money will become the norm this decade. Banks that build the capability to work with stablecoins, tokenized deposits, and CBDCs seamlessly will be best positioned to compete for customers and assets in a digital age.

Contact our team today to set your stablecoin strategy in motion.

Related Articles